corrpdf

corrpdf computes correlation coefficient probability density function

Syntax

y=corrpdf(r, rho, n)example

Examples

Related Examples

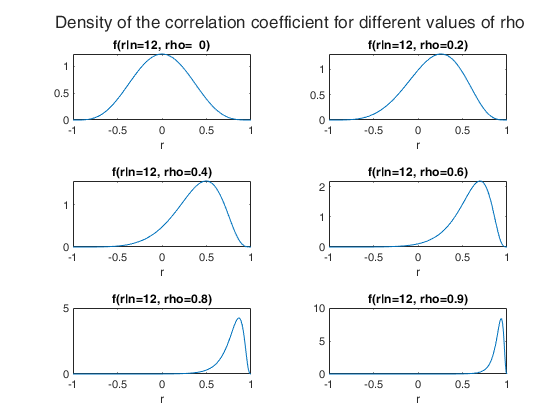

Show density of r given different values for rho.

Show density of r given different values for rho.

Show density of r given different values for rho.

x=-1:0.01:1;

rho=[0:0.2:0.8 0.9]';

n=12;

rhos=num2str(rho);

ns=num2str(n);

close all

for i=1:length(rho)

nexttile

dens=corrpdf(x,rho(i),n);

plot(x,dens)

title(['f(r|n=' ns ', rho=' rhos(i,:) ')'])

xlabel("r")

end

sgtitle('Density of the correlation coefficient for different values of rho')

An example where rho is not scalar.

An example where rho is not scalar.

x=0.3;

rho=(0:0.1:0.8)';

n=12;

xs=string(x);

rhos=string(rho);

ns=string(n);

Dens=corrpdf(x,rho,n);

nameRows="f(r="+xs+"|rho="+ rhos+ ", n="+ ns+ ")=";

nameRowsT=array2table(Dens,"RowNames",nameRows);

disp(nameRowsT)

Dens

________

f(r=0.3|rho=0, n=12)= 0.84417

f(r=0.3|rho=0.1, n=12)= 1.1002

f(r=0.3|rho=0.2, n=12)= 1.2924

f(r=0.3|rho=0.3, n=12)= 1.3543

f(r=0.3|rho=0.4, n=12)= 1.2404

f(r=0.3|rho=0.5, n=12)= 0.95764

f(r=0.3|rho=0.6, n=12)= 0.58395

f(r=0.3|rho=0.7, n=12)= 0.24783

f(r=0.3|rho=0.8, n=12)= 0.054814

Input Arguments

Output Arguments

References

Das Gupta, S. (1980). Distribution of the Correlation Coefficient, in: Fienberg, S.E., Hinkley, D.V. (eds) R.A. Fisher: An Appreciation, Lecture Notes in Statistics, vol 1. Springer, New York, NY.

Acknowledgements

For additional information see https://mathworld.wolfram.com/CorrelationCoefficientBivariateNormalDistribution.html This function follows the lines of MATLAB code developed by Xu Cui, and the file exchange submission Joshua Carmichael (2022). sample correlation distribution function https://www.mathworks.com/matlabcentral/fileexchange/45785-sample-correlation-distribution-function/