msdcutoff

Mahalanobis Squared Distance cutoff

Description

Examples

Related Examples

cutoff values for robust squared Mahalanobis distances.

cutoff values for robust squared Mahalanobis distances.

cutoff values for robust squared Mahalanobis distances.

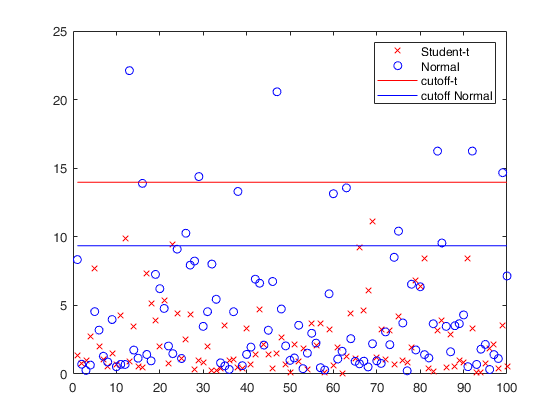

n = 100;

v = 3;

nu = 5;

conflev = 0.975;

% sample from the T

Yt = random('T',nu,[n,v]);

Yn = random('Normal',0,1,[n,v]);

% mcd with the T-model

RAWt = mcd(Yt,'modelT',nu,'plots',0);

% mcd with the Normal-model

RAWn = mcd(Yn,'plots',0);

% T-cutoff

cutoffT = msdcutoff(conflev,v,nu);

% Normal-cutoff

cutoffN = msdcutoff(conflev,v);

plot(1:n,RAWt.md,'xr' , 1:n,RAWn.md,'ob');

hold on;

line([1 , n] , [cutoffT , cutoffT] , 'Color', 'r');

line([1 , n] , [cutoffN , cutoffN] , 'Color', 'b');

legend({'Student-t','Normal','cutoff-t','cutoff Normal'});Total estimated time to complete MCD: 0.24 seconds Total estimated time to complete MCD: 0.10 seconds

Input Arguments

Output Arguments

More About

References

Gnanadesikan, R. and Kettenring, J. R. (1972), Robust estimates, residuals, and outlier detection with multiresponse data. Biometrics, 28:81–124.

Barabesi, L. and Cerioli, A. and García-Escudero, L.A. and Mayo-Iscar, A. (2023), Trimming heavy-tailed multivariate data. Submitted.

Mardia, K. and Kent, J. and Bibby, J. (1979), Multivariate Analysis, Academic Press, New York.

Rousseeuw, P.J. and Van Driessen, K. (1999), A fast algorithm for the minimum covariance determinant estimator, Technometrics, 41:212-223.

Maronna, R.A., Martin D. and Yohai V.J. (2006), "Robust Statistics, Theory and Methods", Wiley, New York.