twdpdf

twdpdf computes the probability density function of the Tweedie distribution.

Syntax

pdf=twdpdf(x,alpha,theta,delta)example

Description

Examples

Related Examples

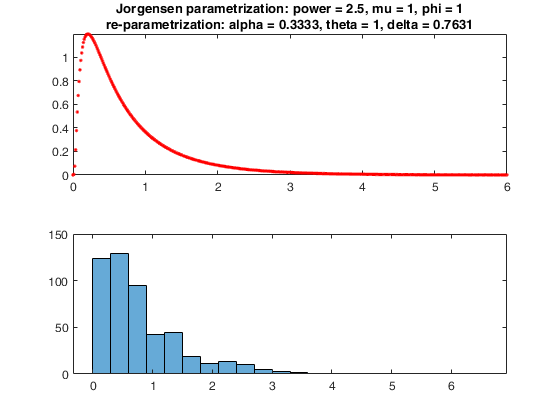

Check consistency with R theedie package.

Check consistency with R theedie package.

Check consistency with R theedie package.Note that the package adopts the parametrization of Jorgensen (1987), which introduces the Tweedie distribution as a special case of the exponential dispersion model.

% In the R tweedie package, the parameters are:

% p = vector of probabilities;

% n = the number of observations;

% xi = the value of xi such that the variance is $var(Y)=\phi \mu^{xi}$;

% power = a synonym for xi

% mu = the mean

% phi = the dispersion

% # R code

% power <- 2.5

% mu <- 1

% phi <- 1

% y <- seq(0, 6, length=500)

% fy <- dtweedie( y=y, power=power, mu=mu, phi=phi)

% plot(y, fy, type="l", lwd=2, ylab="Density")

% # Compare to the saddlepoint density

% f.saddle <- dtweedie.saddle( y=y, power=power, mu=mu, phi=phi)

% lines( y, f.saddle, col=2 )

% legend("topright", col=c(1,2), lwd=c(2,1),

% legend=c("Actual","Saddlepoint") )

% parameter values in Jorgensen parametrization

power = 2.5;

mu = 1 ;

phi = 1 ;

% reparametrization

alpha = (power-2)/(power-1);

theta = phi*mu;

delta = (phi/(power-1))^(1/(power-1));

% pdf

y = linspace(0,6,500);

pdf = twdpdf(y,alpha,theta,delta);

figure;

subplot(2,1,1);

plot(y,pdf,'r.');

title({'Jorgensen parametrization: power = 2.5, mu = 1, phi = 1' , ...

're-parametrization: alpha = 0.3333, theta = 1, delta = 0.7631'});

Y = twdrnd(alpha,theta,delta,500);

subplot(2,1,2);

histogram(Y);

Input Arguments

Output Arguments

More About

References

Tweedie, M. C. K. (1984), An index which distinguishes between some important exponential families, "in Statistics: Applications and New Directions, Proceedings of the Indian Statistical Institute Golden Jubilee International Conference (J.K. Ghosh and J. Roy, eds.), Indian Statistical Institute, Calcutta", pp. 579-604.