FE_int_vol_Fejer

FE_int_vol_Fejer computes the integrated variance from a diffusion process via the Fourier estimator using Fejer kernel

Description

FE_int_vol_Fejer computes the integrated variance of univariate timeseries data from a diffusion process by the Fourier estimator with Fejer kernel

FE_int_vol_Fejer called with optional input argument N.ivar

=FE_int_vol_Fejer(x,

t,

Name, Value)

Examples

Example of call of FE_int_vol_Fejer with just two input arguments.

Example of call of FE_int_vol_Fejer with just two input arguments.

Example of call of FE_int_vol_Fejer with just two input arguments.The following example calculates the integrated variance from a vector x of discrete observations of a univariate diffusion process

n=1000; dt=1/n; t=0:dt:1; x=randn(n,1)*sqrt(dt); x=[0;cumsum(x)]; ivar=FE_int_vol_Fejer(x,t); disp(['The value of the integrated variance is: ' num2str(ivar)])

The value of the integrated variance is: 0.97166

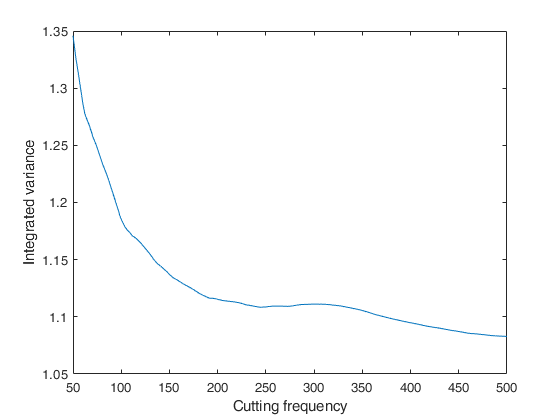

FE_int_vol_Fejer called with optional input argument N.

FE_int_vol_Fejer called with optional input argument N.Analysis of the change of the integrated variance estimates of a univariate diffusion process as a function of the different values of the cutting frequency.

n=1000;

dt=1/n; t=0:dt:1;

x=randn(n,1)*sqrt(dt); x=[0;cumsum(x)];

cuttingfreq=(50:500)';

l=length(cuttingfreq);

Ivar=zeros(l,1);

for i=1:l

ivar=FE_int_vol_Fejer(x,t,'N',cuttingfreq(i));

Ivar(i)=ivar;

end

plot(cuttingfreq,Ivar)

xlabel('Cutting frequency')

ylabel('Integrated variance')

Input Arguments

Output Arguments

More About

References

Mancino, M.E., Recchioni, M.C., Sanfelici, S. (2017), Fourier-Malliavin Volatility Estimation. Theory and Practice, "Springer Briefs in Quantitative Finance", Springer.