Heston1D

Heston1D simulates observations and instantaneous variances from the Heston model

Syntax

Description

Heston1D simulates, using the Euler–Maruyama method, observations and instantaneous variances from the model by [S. Heston, The Review of Financial Studies, Vol. 6, No. 2, 1993].

Example of call of Heston1D for obtaining process observations only.x

=Heston1D(T,

n,

parameters,

rho,

x0,

V0)

Examples

Example of call of Heston1D for obtaining process observations only.

Example of call of Heston1D for obtaining process observations only.

Example of call of Heston1D for obtaining process observations only.Generates observations from the Heston model.

T=1;

n=23400;

parameters=[0,0.4,2,1];

rho=-0.5;

x0=log(100);

V0=0.4;

x = Heston1D(T,n,parameters,rho,x0,V0);

figure

plot(x)

ylabel('Observations')

title('Heston model')

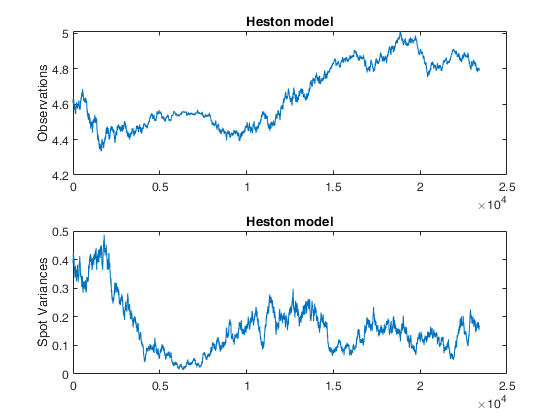

Example of call of Heston1D for obtaning process observations and volatility values.

Example of call of Heston1D for obtaning process observations and volatility values.Generates observations and volatilities from the Heston model.

T=1;

n=23400;

parameters=[0,0.4,2,1];

rho=-0.5;

x0=log(100);

V0=0.4;

[x,V] = Heston1D(T,n,parameters,rho,x0,V0);

figure

subplot(2,1,1)

plot(x)

ylabel('Observations')

title('Heston model')

subplot(2,1,2)

plot(V)

ylabel('Spot Variances')

title('Heston model')

Example of call of Heston1D for obtaning process observations, volatility values and sampling times.

Example of call of Heston1D for obtaning process observations, volatility values and sampling times.Generates observations, volatilities and sampling times from the Heston model.

T=1;

n=23400;

parameters=[0,0.4,2,1];

rho=-0.5;

x0=log(100);

V0=0.4;

[x,V,t] = Heston1D(T,n,parameters,rho,x0,V0);

figure

subplot(2,1,1)

plot(t,x)

xlabel('Time')

ylabel('Observations')

title('Heston model')

subplot(2,1,2)

plot(t,V)

xlabel('Time')

ylabel('Spot Variances')

title('Heston model')

Input Arguments

Output Arguments

More About

References

Heston, S. (1993), A closed-form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies, Vol. 6, No. 2.