CEVmodel

CEVmodel computes price and instantaneous variance processes from the CEV model

Description

CEVmodel computes price and instantaneous variance for the Constant Elasticity of Variance model [S. Beckers, The Journal of Finance, Vol. 35, No. 3, 1980] via Euler method

Examples

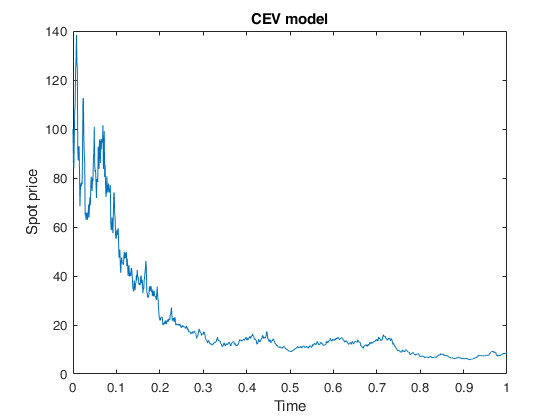

Example of call of CEVmodel providing only price values.

Example of call of CEVmodel providing only price values.

Example of call of CEVmodel providing only price values.Generates spot prices for the CEV model at times t.

n=1000; dt=1/n;

t=0:dt:1; % discrete time grid

x=100; % initial price value

S=CEVmodel(t,x); % spot prices

plot(t,S)

xlabel('Time')

ylabel('Spot price')

title('CEV model')

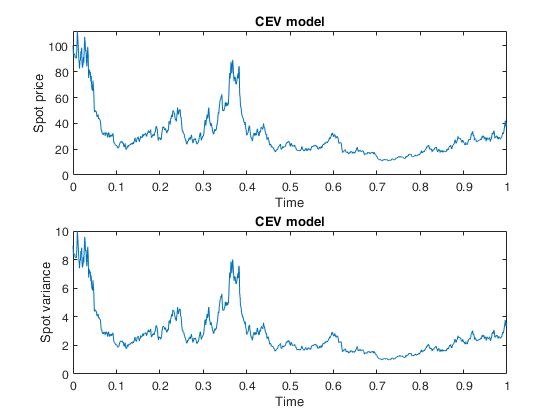

Example of call of CEVmodel providing both price and variance values.

Example of call of CEVmodel providing both price and variance values.Generates price and instantaneous variance values for the CEV model at times t.

n=1000; dt=1/n;

t=0:dt:1; % discrete time grid

x=100; % initial price value

[S,A]=CEVmodel(t,x); % spot prices and variance

subplot(2,1,1)

plot(t,S)

xlabel('Time')

ylabel('Spot price')

title('CEV model')

subplot(2,1,2)

plot(t,A)

xlabel('Time')

ylabel('Spot variance')

title('CEV model')