FE_spot_vol

FE_spot_vol estimates the instantaneous variance of a diffusion process by the Fourier estimator with Dirichlet kernel

Syntax

Description

FE_spot_vol called with optional input argument N and M.spotvar

=FE_spot_vol(x,

t,

Name, Value)

Examples

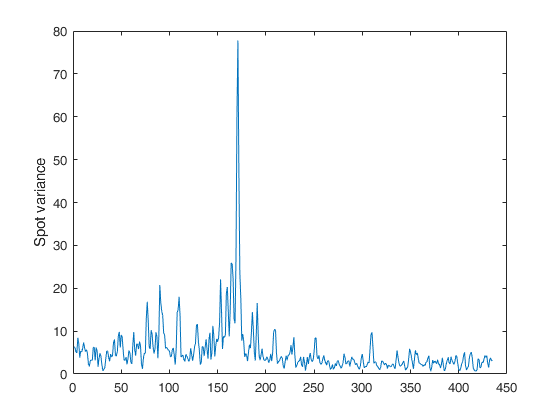

Example of call of FE_spot_vol with just two input arguments.

Example of call of FE_spot_vol with just two input arguments.

Example of call of FE_spot_vol with just two input arguments.Generates price and instantaneous variance from the Constant Elasticity of Variance model [S. Beckers, The Journal of Finance, Vol. 35, No. 3, 1980] and estimates the instantaneous variance via the Fourier method.

n=1000; T=1; t=0:T/n:T; S0=100;

[S,sigma]=CEVmodel(t,S0); % data generation

x=log(S); % log-price

spotvar=FE_spot_vol(x,t);

plot(spotvar(2:end-1))

ylabel('Spot variance')

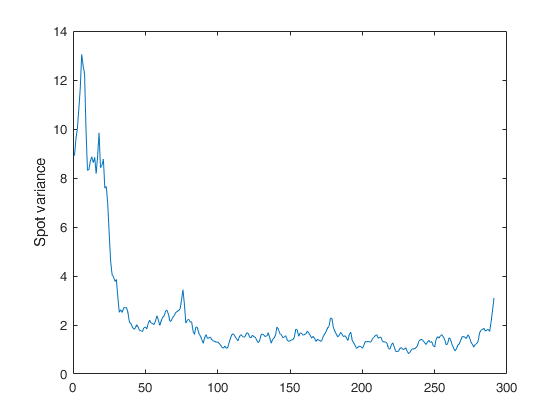

FE_spot_vol called with optional input argument N and M.

FE_spot_vol called with optional input argument N and M.Generates price and instantaneous variance from the Constant Elasticity of Variance model [S. Beckers, The Journal of Finance, Vol. 35, No. 3, 1980] and estimates the instantaneous variance via the Fourier method.

n=21600; T=1; t=0:T/n:T; S0=100;

[S,sigma]=CEVmodel(t,S0); % data generation

x=log(S); % log-price

N=floor(n/2); M=floor(n^0.5); % cutting frequencies

spotvar=FE_spot_vol(x,t,'N',N,'M',M);

plot(spotvar(2:end-1))

ylabel('Spot variance')

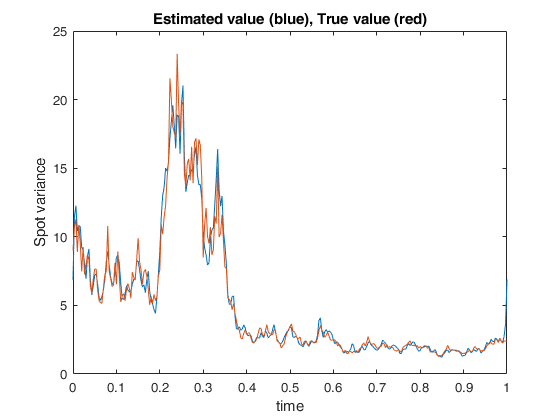

Example of call of FE_spot_vol providing both estimation values and times.

Example of call of FE_spot_vol providing both estimation values and times.Generates price and instantaneous variance from the Constant Elasticity of Variance model [S. Beckers, The Journal of Finance, Vol. 35, No. 3, 1980] and estimates the instantaneous variance via the Fourier method.

n=21600; T=1; t=0:T/n:T; S0=100;

[S,sigma]=CEVmodel(t,S0); % data generation

x=log(S); % log-price

N=floor(n/2); M=150; % cutting frequencies

[spotvar,tau]=FE_spot_vol(x,t,'N',N,'M',M);

plot(tau,spotvar)

xlabel('time')

hold on; plot(tau,sigma(1:n/(2*M):end));

ylabel('Spot variance')

title('Estimated value (blue), True value (red)')

Input Arguments

Output Arguments

More About

References

Mancino, M.E., Recchioni, M.C., Sanfelici, S. (2017), Fourier-Malliavin Volatility Estimation. Theory and Practice, "Springer Briefs in Quantitative Finance", Springer.