|

FSRaddt |

FSRBbsb |

|

FSRB

FSRB gives an automatic outlier detection procedure in Bayesian linear regression

Description

Examples

FSRB with optional arguments.

FSRB with optional arguments.

FSRB with optional arguments.

load hprice.txt;

n=size(hprice,1);

y=hprice(:,1);

X=hprice(:,2:5);

% set \beta components

beta0=0*ones(5,1);

beta0(2,1)=10;

beta0(3,1)=5000;

beta0(4,1)=10000;

beta0(5,1)=10000;

% \tau

s02=1/4.0e-8;

tau0=1/s02;

% R prior settings

R=2.4*eye(5);

R(2,2)=6e-7;

R(3,3)=.15;

R(4,4)=.6;

R(5,5)=.6;

R=inv(R);

% define a Bayes structure with previous data

n0=5;

bayes=struct;

bayes.R=R;

bayes.n0=n0;

bayes.beta0=beta0;

bayes.tau0=tau0;

intercept=true;

% function call

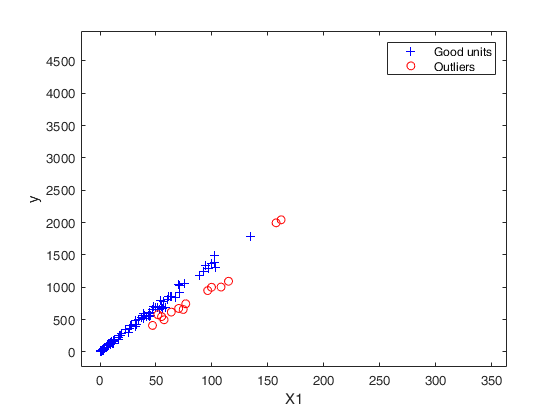

out=FSRB(y,X,'bayes',bayes,'msg',0,'plots',1,'init',round(n/2),'intercept', intercept)

out =

struct with fields:

ListOut: [55 93 95 103 104 129 130 162 210 330 331 338 … ] (1×18 double)

outliers: [55 93 95 103 104 129 130 162 210 330 331 338 … ] (1×18 double)

mdr: [273×2 double]

Un: [273×11 double]

nout: [2×5 double]

beta: [5×1 double]

scale: 1.4951e+04

class: 'FSRB'

Related Examples

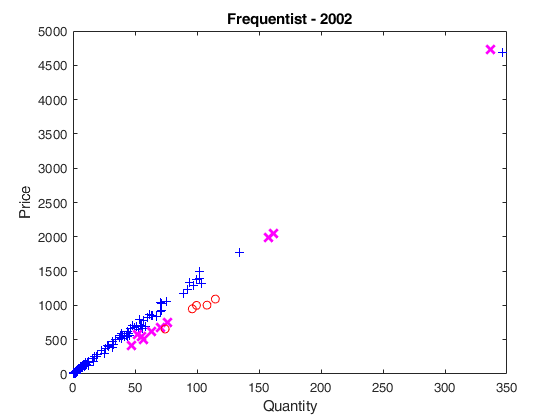

Example on Fishery dataset (analysis with intercept).

Example on Fishery dataset (analysis with intercept).nsamp is the number of subsamples to use in the frequentist analysis of first year, in order to find initial subset using LMS.

close all

nsamp=3000;

% threshold to be used to increase subset of good units

threshold=300;

bonflev=0.99; % Bonferroni confidence level to be used for first year

bonflevB=0.99; % Bonferroni confidence level to be used for subsequent years

% Load 2002 Fishery dataset

Fishery2002=load('Fishery2002.txt');

y02=Fishery2002(:,3);

X02=Fishery2002(:,2);

n02=length(y02);

seq02=1:n02;

% frequentist Forward Search, 1st year

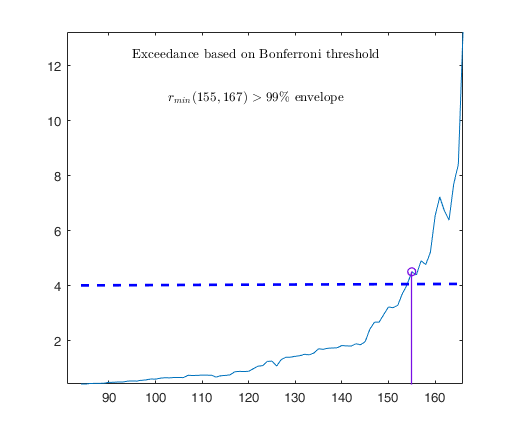

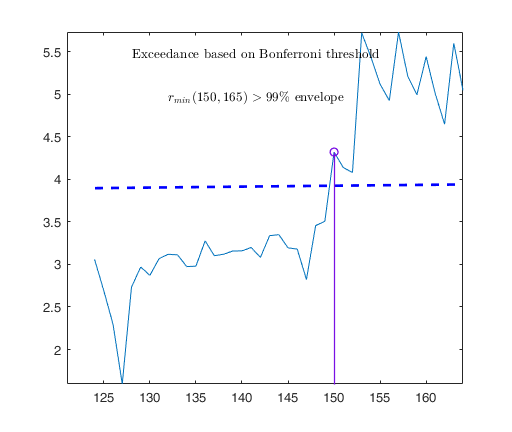

[out02]=FSR(y02,X02,'nsamp',nsamp,'plots',1,'msg',0,'init',round(n02*3/4),'bonflev',bonflev);

% In what follows

% g stands for good units

% i stand for intermediate units (i.e. units whose raw residual is smaller

% than threshold)

% o stands for outliers

% gi stands for good +intermediate units

% u02g = good units

% n02g = number of good units

u02g=setdiff(seq02,out02.ListOut);

n02g=length(u02g);

X02g=[ones(length(u02g),1) X02(u02g,:)];

y02g=y02(u02g);

% b02g = regression coefficients just using g units

b02g=X02g\y02g;

% res02 = squared raw residuals for all units using b02g

res02=(y02-[ones(length(X02),1) X02]*b02g).^2;

res02o=res02(out02.ListOut);

% sel= boolean vector which is true for the intermediate units

% (units whose squared residual is below the threshold)

sel=res02o<threshold^2;

% u02i = vector containing intermediate units (that is outliers whose

% residual is smaller than threshold)

u02i=out02.ListOut(sel);

% u02o = vector containing outliers whose residual is out of the threshold

u02o=out02.ListOut(~sel);

% u02gi = g + i units

if ~isempty(u02i)

u02gi=[u02g u02i];

else

u02gi=u02g;

end

% n02gi = number of good + intermediate units

n02gi=length(u02gi);

% plotting section

hold('off')

% good units, plotted as (+)

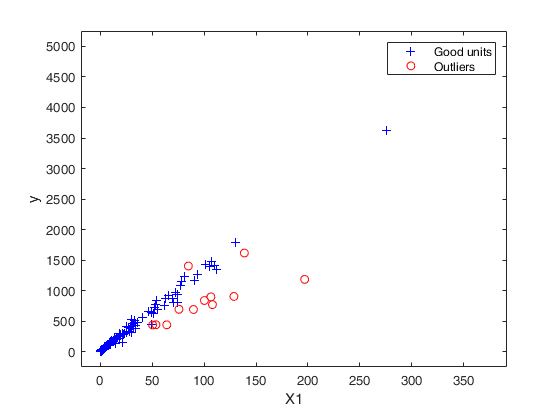

plot(X02(u02g)',y02(u02g)','Marker','+','LineStyle','none','Color','b')

hold('on')

% intermediate units plotted as (X)

plot(X02(u02i)',y02(u02i)','Marker','X','MarkerSize',9,'LineWidth',2,'LineStyle','none','Color','m')

% outliers, plotted as (O)

plot(X02(u02o)',y02(u02o)','Marker','o','LineStyle','none','Color','r')

xlabel('Quantity');

ylabel('Price');

title('Frequentist - 2002');

% S202gi = estimated of sigma^2 using g+i units

S202gi=sum(res02(u02gi))/(n02gi-2);

% X02gi = X matrix referred to good + intermediate units

X02gi=[ones(n02gi,1) X02(u02gi,:)];

% y02gi = y vector referred to good + intermediate units

y02gi=y02(u02gi);

% bayes = structure which contains prior information to be used in year

% 2003

bayes=struct;

bayes.beta0=b02g; % beta prior is beta based on g units

tau0=1/S202gi; % tau0 is based on g + i units

bayes.tau0=tau0;

R=X02g'*X02g; % R is based on g units

bayes.n0=n02gi; % n0 is based on g + i units

bayes.R=R;

% 2003

% Load 2003 Fishery dataset

Fishery2003=load('Fishery2003.txt');

y03=Fishery2003(:,3);

X03=Fishery2003(:,2);

n03=length(y03);

seq03=1:n03;

% Bayesian Forward Search, 2nd year

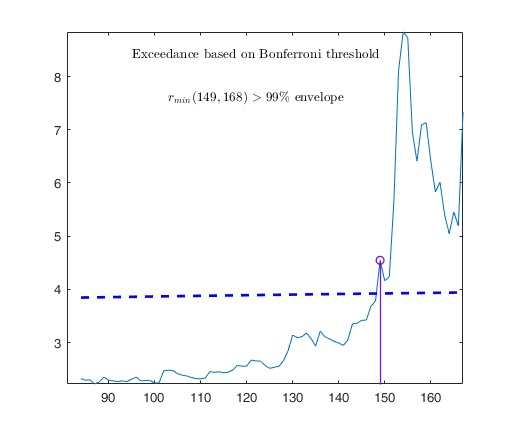

out03=FSRB(y03,X03,'bayes',bayes,'msg',0,'plots',1,'init',round(n03/2),'bonflev',bonflevB);

u03g=setdiff(seq03,out03.ListOut);

n03g=length(u03g);

% compute beta coefficient for year 2003 just using good units

X03g=[ones(n03g,1) X03(u03g,:)];

y03g=y03(u03g);

b03g=X03g\y03g;

res03=(y03-[ones(length(X03),1) X03]*b03g).^2;

res03o=res03(out03.ListOut);

sel=res03o<threshold^2;

% u03i = units to add to the good units subset (intermediate units)

u03i=out03.ListOut(sel);

% u03o = outliers out of the threshold

u03o=out03.ListOut(~sel);

if ~isempty(u03i)

u03gi=[u03g u03i];

else

u03gi=u03g;

end

n03gi=length(u03gi);

X03gi=[ones(n03gi,1) X03(u03gi,:)];

y03gi=y03(u03gi,:);

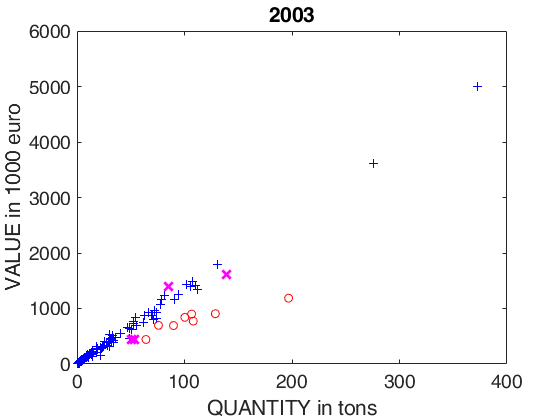

% plotting section

hold('off')

% good units, plotted as (+)

plot(X03(u03g)',y03(u03g)','Marker','+','LineStyle','none','Color','b')

hold('on')

% units below the threshold, plotted as (X)

plot(X03(u03i)',y03(u03i)','Marker','X','MarkerSize',9,'LineWidth',2,'LineStyle','none','Color','m')

% outliers, plotted as (O)

plot(X03(u03o)',y03(u03o)','Marker','o','LineStyle','none','Color','r')

set(gca,'FontSize',14)

xlabel('QUANTITY in tons')

ylabel('VALUE in 1000 euro')

title('2003');

% Definition of bayes structure (based on 2002 and 2003)

bayes=struct;

X02gX03g=[X02g; X03g];

y02gy03g=[y02g; y03g];

n02gn03g=n02g+n03g;

% b0203g prior estimate of beta for year 2004 is computed using good units

% for years 2002 and 2003

b0203g=X02gX03g\y02gy03g;

bayes.beta0=b0203g;

% R is just referred to good units for years 2002 and 2003

R=X02gX03g'*X02gX03g;

bayes.R=R;

% n0 is referred to g + i units in 2002 and 2003

bayes.n0=n02gi+n03gi;

X02giX03gi=[X02gi; X03gi];

y02giy03gi=[y02gi; y03gi];

% n02gin03gi = number of g+i units in 2002 and 2003

n02gin03gi=n02gi+n03gi;

% res = residuals for g+i units using b0203g

res=y02giy03gi-X02giX03gi*b0203g;

S203gi=sum(res.^2)/(n02gin03gi-2);

% estimate of tau is based on g + i units

tau0=1/S203gi;

bayes.tau0=tau0;

% Load 2004 Fishery dataset

Fishery2004=load('Fishery2004.txt');

y04=Fishery2004(:,3);

X04=Fishery2004(:,2);

n04=length(y04);

seq04=1:n04;

% Bayesian Forward Search, 3rd year

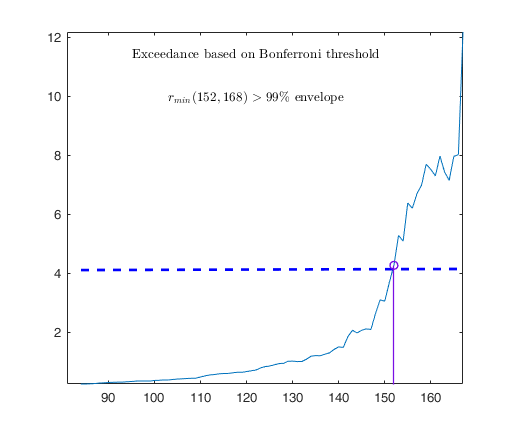

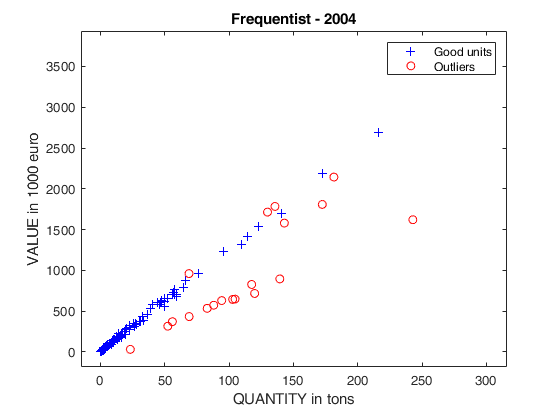

out04=FSRB(y04,X04,'bayes',bayes,'msg',0,'plots',1,'init',round(n04/2),'bonflev',bonflevB);

u04g=setdiff(seq04,out04.ListOut);

n04g=length(u04g);

X04g=[ones(n04g,1) X04(u04g,:)];

y04g=y04(u04g);

% b04g = beta based on good units for year 2004

b04g=X04g\y04g;

res04=(y04-[ones(length(X04),1) X04]*b04g).^2;

% res04o squared residuals for the tentative outliers

res04o=res04(out04.ListOut);

% we keep statistical units below the threshold

sel=res04o<threshold^2;

% u04i = units to add to the good units subset (intermediate units)

u04i=out04.ListOut(sel);

% u04o = units outliers out of the threshold

u04o=out04.ListOut(~sel);

if ~isempty(u04i)

u04gi=[u04g u04i];

else

u04gi=u04g;

end

n04gi=length(u04gi);

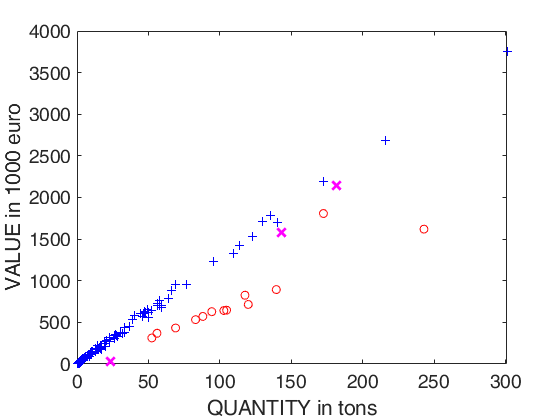

% plotting section

hold('off')

% good units, plotted as (+)

plot(X04(u04g)',y04(u04g)','Marker','+','LineStyle','none','Color','b')

hold('on')

% units below the threshold, plotted as (X)

plot(X04(u04i)',y04(u04i)','Marker','X','MarkerSize',9,'LineWidth',2,'LineStyle','none','Color','m')

% outliers, plotted as (O)

plot(X04(u04o)',y04(u04o)','Marker','o','LineStyle','none','Color','r')

set(gca,'FontSize',14)

xlabel('QUANTITY in tons')

ylabel('VALUE in 1000 euro')

% frequentist Forward Search, 3rd year

out04=FSR(y04,X04,'nsamp',nsamp,'plots',1,'msg',0,'init',round(n04/2),'bonflev',bonflev);

xlabel('QUANTITY in tons')

ylabel('VALUE in 1000 euro')

title('Frequentist - 2004');

Example on Fishery dataset (analysis without the intercept).

Example on Fishery dataset (analysis without the intercept).

close all

% nsamp is the number of subsamples to use in the frequentist analysis of first

% year, in order to find initial subset using LMS.

nsamp=3000;

% threshold to be used to increase subset of good units

threshold=300;

bonflev=0.99; % Bonferroni confidence level

% Load 2002 Fishery dataset

Fishery2002=load('Fishery2002.txt');

y02=Fishery2002(:,3);

X02=Fishery2002(:,2);

n02=length(y02);

seq02=1:n02;

% frequentist Forward Search, 1st year (regression without intercept)

[out02]=FSR(y02,X02,'intercept',false,'nsamp',nsamp,'plots',1,'msg',0,'init',round(n02*3/4),'bonflev',bonflev);

% In what follows

% g stands for good units

% i stand for intermediate units (i.e. units whose raw residual is smaller

% than threshold)

% o stands for outliers

% gi stands for good +intermediate units

% u02g = good units

% n02g = number of good units

u02g=setdiff(seq02,out02.ListOut);

X02g=X02(u02g,:);

y02g=y02(u02g);

% b02g = regression coefficients just using g units

% Note that b02g is a scalar because the intercept has not been added

b02g=X02g\y02g;

% res02 = squared raw residuals for all units using b02g

res02=(y02-X02*b02g).^2;

res02o=res02(out02.ListOut);

% sel= boolean vector which is true for the intermediate units

% (units whose squared residual is below the threshold)

sel=res02o<threshold^2;

% u02i = vector containing intermediate units (that is outliers whose

% residual is smaller than threshold)

u02i=out02.ListOut(sel);

% u02gi = g + i units

if ~isempty(u02i)

u02gi=[u02g u02i];

else

u02gi=u02g;

end

% n02gi = number of good + intermediate units

n02gi=length(u02gi);

% S202gi = estimated of sigma^2 using g+i units

S202gi=sum(res02(u02gi))/(n02gi-1);

% bayes = structure which contains prior information to be used in year

% 2003

bayes=struct;

bayes.beta0=b02g; % beta prior is beta based on g units

tau0=1/S202gi; % tau0 is based on g + i units

bayes.tau0=tau0;

R=X02g'*X02g; % R is based on g units

bayes.n0=n02gi; % n0 is based on g + i units

bayes.R=R;

% 2003

% Load 2003 Fishery dataset

Fishery2003=load('Fishery2003.txt');

y03=Fishery2003(:,3);

X03=Fishery2003(:,2);

n03=length(y03);

% Run Bayesian Forward Search for the 2nd year using the prior based on

% the first year.

out03=FSRB(y03,X03,'bayes',bayes,'msg',0,'plots',1,'init',round(n03/2),'bonflev',bonflev,'intercept',false);

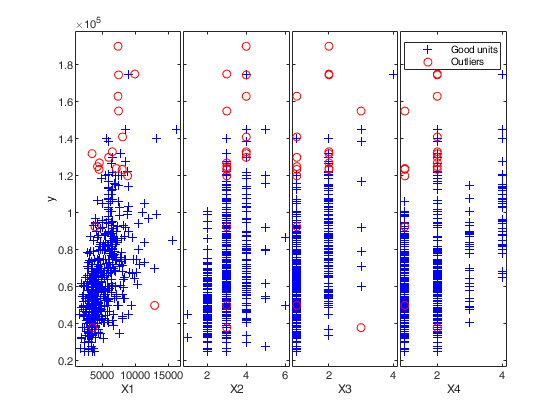

Outlier detection for Bank-Profit data.

Outlier detection for Bank-Profit data.

XX=load('BankProfit.txt');

R=load('BankProfitR.txt');

X=XX(:,1:end-1);

y=XX(:,end);

% Load prior information

beta0=zeros(10,1);

beta0(1,1)=-0.5;

beta0(2,1)=9.1; % Number of products (NUMPRO)

beta0(3,1)=0.001; % direct revenues (DIRREV)

beta0(4,1)=0.0002; % indirect revenues (INDREV)

beta0(5,1)=0.002; % savings accounts SAVACC

beta0(6,1)=0.12; % number of operations NUMOPE

beta0(7,1)=0.0004; % total amount of operations TOTOPE

beta0(8,1)=-0.0004; % Bancomat POS

beta0(9,1)=1.3; % Number of cards NUMCAR

beta0(10,1)=0.00004; % Amount in cards TOTCAR

% \tau

s02=10000;

tau0=1/s02;

% number of obs in which prior was based

n0=1500;

bayes=struct;

bayes.R=R;

bayes.n0=n0;

bayes.beta0=beta0;

bayes.tau0=tau0;

intercept=true;

n=length(y);

out=FSRB(y,X,'bayes',bayes,'msg',1,'plots',1,...

'init',round(n/2),'xlim',[1700 1905],'ylim',[2 4]);

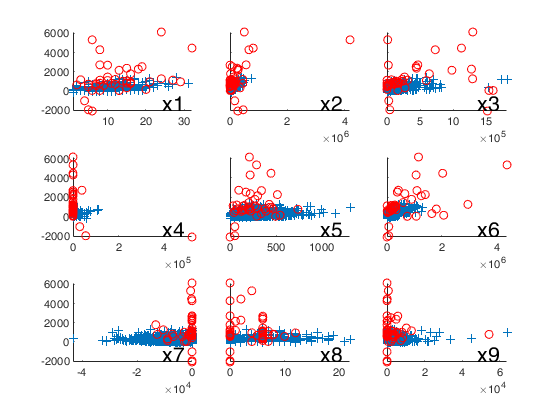

% Plot the outliers with a different symbol using a 3x3 layout.

selout=out.ListOut;

selin=setdiff(1:n,selout);

close all

% just in case user has additional function subtightplot

% http://www.mathworks.com/matlabcentral/fileexchange/39664-subtightplot

make_it_tight = false;

if make_it_tight == true && exist('subtightplot','file') ==2

subplot = @(m,n,p) subtightplot (m, n, p, [0.05 0.025], [0.1 0.01], [0.1 0.01]);

else

clear subplot;

end

% sel = panels in which yticks do not have to be removed

sel=[1 4 7];

miny=min(y);

maxy=max(y);

for j=1:9

subplot(3,3,j)

hold('on')

plot(X(selin,j),y(selin),'+')

plot(X(selout,j),y(selout),'ro')

ylim([miny maxy])

xlim([min(X(:,j)) max(X(:,j))])

if isempty(intersect(j,sel))

set(gca,'YTickLabel','')

end

% Add on the plot the variable name

text(0.75,0.1,['x' num2str(j)],'Units','normalized','FontSize',16)

end

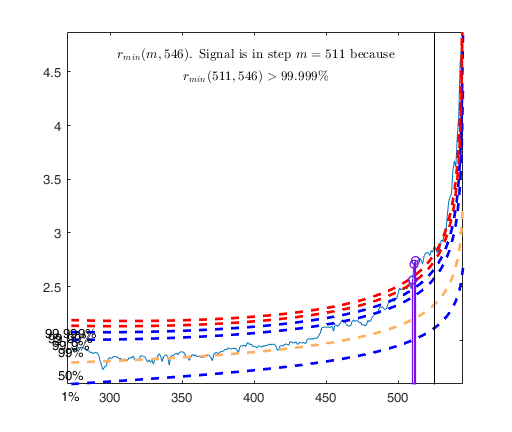

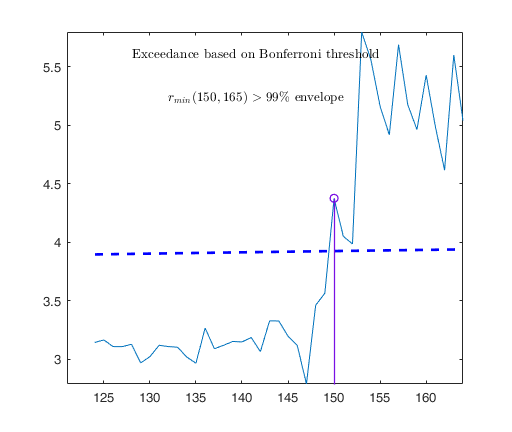

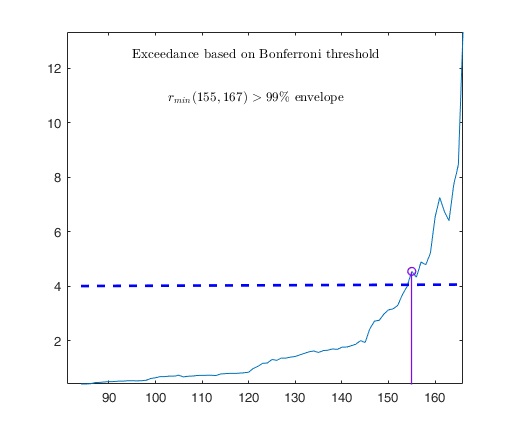

Observed curve of r_min is at least 10 times greater than 99.99% envelope

--------------------------------------------------

-------------------------

Signal detection loop

Tentative signal in central part of the search: step m=1830 because

rmin(1830,1903)>99.999%

-------------------

Signal validation exceedance of upper envelopes

Validated signal

-------------------------------

Start resuperimposing envelopes from step m=1829

Superimposition stopped because r_{min}(1851,1859)>99.9% envelope

Subsample of 1858 units is homogeneous

----------------------------

Final output

Number of units declared as outliers=45

Summary of the exceedances

1 99 999 9999 99999

838 77 76 73 73

Input Arguments

Output Arguments

References

Chaloner, K. and Brant, R. (1988), A Bayesian Approach to Outlier Detection and Residual Analysis, "Biometrika", Vol. 75, pp. 651-659.

Riani, M., Corbellini, A. and Atkinson, A.C. (2018), Very Robust Bayesian Regression for Fraud Detection, "International Statistical Review", http://dx.doi.org/10.1111/insr.12247

Atkinson, A.C., Corbellini, A. and Riani, M., (2017), Robust Bayesian Regression with the Forward Search: Theory and Data Analysis, "Test", Vol. 26, pp. 869-886, https://doi.org/10.1007/s11749-017-0542-6

|

|

FSRaddt |

FSRBbsb |

|

|

|

Functions |

|

• The developers of the toolbox • The forward search group • Terms of Use • Acknowledgments