|

FSRBbsb |

FSRBmdr |

|

FSRBeda

FSRBeda enables to monitor several quantities in each step of the Bayesian search

Description

Examples

Related Examples

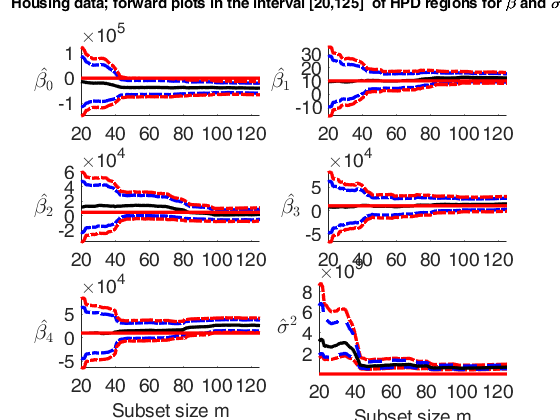

Plot posterior estimates of beta and sigma2.

Plot posterior estimates of beta and sigma2.

Plot posterior estimates of beta and sigma2.Plot posterior estimates of beta and sigma2 in the interval (subset size) [20 125].

% In this example, for the house price data, we monitor the forward plots

% of the parameters of the linear model, adding 95% and 99% HPD

% regions. The first 8 panels refer to the elements of $\beta_1$

% and the bottom right-hand panel refer to the estimate of sigma2.

% The horizontal lines correspond to prior values.

% The vertical lines refer to the step prior to the introduction of the first outlier

% init = point to start monitoring diagnostics along the FS

% run routine FSRB in order to find the outliers automatically.

load hprice.txt;

% setup parameters

n=size(hprice,1);

y=hprice(:,1);

X=hprice(:,2:5);

bayes=struct;

n0=5;

bayes.n0=n0;

% set \beta components

beta0=0*ones(5,1);

beta0(2,1)=10;

beta0(3,1)=5000;

beta0(4,1)=10000;

beta0(5,1)=10000;

bayes.beta0=beta0;

% \tau

s02=1/4.0e-8;

tau0=1/s02;

bayes.tau0=tau0;

% R prior settings

R=2.4*eye(5);

R(2,2)=6e-7;

R(3,3)=.15;

R(4,4)=.6;

R(5,5)=.6;

R=inv(R);

bayes.R=R;

outBA=FSRB(y,X,'bayes',bayes', 'plots',0);

dout=n-length(outBA.ListOut);

% init = initial point to start monitoring

init=20;

xlimL=init; % lower value of xlim

xlimU=125; % upper value of xlim

outBAeda=FSRBeda(y,X,'bayes',bayes,'init',init, 'conflev', [0.95 0.99]);

% Set font size, line width and line style

figure;

lwd=2.5;

FontSize=14;

linst={'-','--',':','-.','--',':'};

for j=1:5

my_subplot=subplot(3,2,j);

hold('on')

% plot 95% and 99% HPD trajectories

plot(outBAeda.beta1(:,1),outBAeda.beta1HPD(:,1:2,j),'LineStyle',linst{4},'LineWidth',lwd,'Color','b')

plot(outBAeda.beta1(:,1),outBAeda.beta1HPD(:,3:4,j),'LineStyle',linst{4},'LineWidth',lwd,'Color','r')

% plot posterior estimate of beta1_j

plot(outBAeda.beta1(:,1),outBAeda.beta1(:,j+1)','LineStyle',linst{1},'LineWidth',lwd,'Color','k')

% Add the horizontal line which corresponds to prior values

xL = get(my_subplot,'XLim');

line(xL,[beta0(j) beta0(j)],'Color','r','LineWidth',lwd);

% Set ylim

ylimU=max([outBAeda.beta1HPD(:,4,j); beta0(j)]);

ylimL=min([outBAeda.beta1HPD(:,3,j); beta0(j)]);

ylim([ylimL ylimU])

% Add vertical line in correspondence of the step prior to the

% entry of the first outlier

line([dout; dout],[ylimL; ylimU],'Color','r','LineWidth',lwd);

% Set xlim

xlim([xlimL xlimU]);

ylabel(['$\hat{\beta_' num2str(j-1) '}$'],'Interpreter','LaTeX','FontSize',20,'rot',-360);

set(gca,'FontSize',FontSize);

if j>4

xlabel('Subset size m','FontSize',FontSize);

end

end

% Subplot associated with the monitoring of sigma^2

subplot(3,2,6);

%figure()

hold('on')

% 99%

plot(outBAeda.sigma21HPD(:,1),outBAeda.sigma21HPD(:,4:5),'LineStyle',linst{4},'LineWidth',lwd,'Color','r')

% 95%

plot(outBAeda.sigma21HPD(:,1),outBAeda.sigma21HPD(:,2:3),'LineStyle',linst{2},'LineWidth',lwd,'Color','b')

% Plot 1\/tau1

plot(outBAeda.S21(:,1),1./outBAeda.S21(:,3),'LineWidth',lwd,'Color','k')

ylabel('$\hat{\sigma}^2$','Interpreter','LaTeX','FontSize',20,'rot',-360);

set(gca,'FontSize',FontSize);

% Set ylim

ylimU=max([outBAeda.sigma21HPD(:,5); s02]);

ylimL=min([outBAeda.sigma21HPD(:,4); s02]);

ylim([ylimL ylimU])

% Set xlim

xlim([xlimL xlimU]);

xL = get(my_subplot,'XLim');

% Add the horizontal line which corresponds to prior value of $\sigma^2$

line(xL,[s02 s02],'Color','r','LineWidth',lwd);

% Add vertical line in correspondence of the step prior to the

% entry of the first outlier

line([dout; dout],[ylimL; ylimU],'Color','r','LineWidth',lwd);

xlabel('Subset size m','FontSize',FontSize);

% Add multiple title

suplabel(['Housing data; forward plots in the interval ['...

num2str(xlimL) ',' num2str(xlimU) ...

'] of HPD regions for \beta and \sigma^2'],'t');

Observed curve of r_min is at least 10 times greater than 99.99% envelope

--------------------------------------------------

-------------------------

Signal detection loop

Tentative signal in central part of the search: step m=511 because

rmin(511,546)>99.99% and rmin(510,546)>99.99% and rmin(512,546)>99.99%

rmin(511,546)>99.999%

-------------------

Signal validation exceedance of upper envelopes

Validated signal

-------------------------------

Start resuperimposing envelopes from step m=510

Superimposition stopped because r_{min}(512,529)>99.9% envelope

Subsample of 528 units is homogeneous

----------------------------

Final output

Number of units declared as outliers=18

Summary of the exceedances

1 99 999 9999 99999

10 64 48 38 29

m=100

m=200

m=300

m=400

m=500

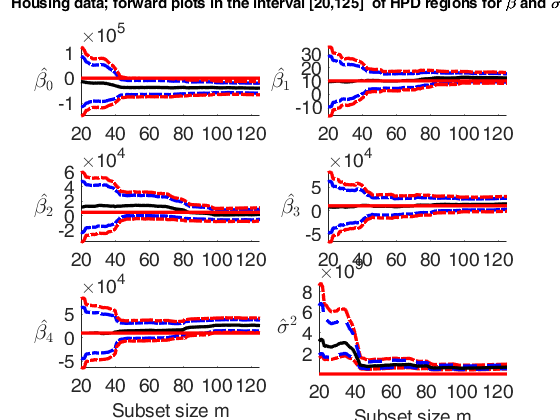

Plot posterior estimates of beta and sigma2 in the last steps.

Plot posterior estimates of beta and sigma2 in the last steps.Plot posterior estimates of beta and sigma2 in the interval (subset size) [250 n+1].

% In this example for the house price data we monitor the forward plots

% of the parameters of the linear model adding 95% and 99% HPD

% regions. The first 8 panels refer to the elements of $\beta_1$

% and the bottom right-hand panel refer to the estimate of sigma2.

% The horizontal lines correspond to prior values.

% The vertical lines refer to the step prior to the introduction of the first outlier

% init = point to start monitoring diagnostics along the FS

% run routine FSRB in order to find the outliers automatically

load hprice.txt;

% setup parameters

n=size(hprice,1);

y=hprice(:,1);

X=hprice(:,2:5);

bayes=struct;

n0=5;

bayes.n0=n0;

% set \beta components

beta0=0*ones(5,1);

beta0(2,1)=10;

beta0(3,1)=5000;

beta0(4,1)=10000;

beta0(5,1)=10000;

bayes.beta0=beta0;

% \tau

s02=1/4.0e-8;

tau0=1/s02;

bayes.tau0=tau0;

% R prior settings

R=2.4*eye(5);

R(2,2)=6e-7;

R(3,3)=.15;

R(4,4)=.6;

R(5,5)=.6;

R=inv(R);

bayes.R=R;

% Automatic outlier detection procedure.

outBA=FSRB(y,X,'bayes',bayes', 'plots',0);

dout=n-length(outBA.ListOut);

% init = initial point to start monitoring

init=250;

xlimL=init; % lower value fo xlim

xlimU=n+1; % upper value of xlim

out=FSRBeda(y,X,'bayes',bayes,'init',init, 'conflev', [0.95 0.99]);

% Set font size, line width and line style

figure;

lwd=2.5;

FontSize=14;

linst={'-','--',':','-.','--',':'};

for j=1:5

my_subplot=subplot(3,2,j);

hold('on')

% plot 95% and 99% HPD trajectories

plot(out.beta1(:,1),out.beta1HPD(:,1:2,j),'LineStyle',linst{4},'LineWidth',lwd,'Color','b')

plot(out.beta1(:,1),out.beta1HPD(:,3:4,j),'LineStyle',linst{4},'LineWidth',lwd,'Color','r')

% plot posterior estimate of beta1_j

plot(out.beta1(:,1),out.beta1(:,j+1)','LineStyle',linst{1},'LineWidth',lwd,'Color','k')

% Add the horizontal line which corresponds to prior values

xL = get(my_subplot,'XLim');

line(xL,[beta0(j) beta0(j)],'Color','r','LineWidth',lwd);

% Set ylim

ylimU=max([out.beta1HPD(:,4,j); beta0(j)]);

ylimL=min([out.beta1HPD(:,3,j); beta0(j)]);

ylim([ylimL ylimU])

% Set xlim

xlim([xlimL xlimU]);

% Add vertical line in correspondence of the step prior to the

% entry of the first outlier

line([dout; dout],[ylimL; ylimU],'Color','r','LineWidth',lwd);

ylabel(['$\hat{\beta_' num2str(j-1) '}$'],'Interpreter','LaTeX','FontSize',20,'rot',-360);

set(gca,'FontSize',FontSize);

if j>4

xlabel('Subset size m','FontSize',FontSize);

end

end

% Subplot associated with the monitoring of sigma^2

subplot(3,2,6);

%figure()

hold('on')

% 99%

plot(out.sigma21HPD(:,1),out.sigma21HPD(:,4:5),'LineStyle',linst{4},'LineWidth',lwd,'Color','r')

% 95%

plot(out.sigma21HPD(:,1),out.sigma21HPD(:,2:3),'LineStyle',linst{2},'LineWidth',lwd,'Color','b')

% Plot 1/tau1

plot(out.S21(:,1),1./out.S21(:,3),'LineWidth',lwd,'Color','k')

ylabel('$\hat{\sigma}^2$','Interpreter','LaTeX','FontSize',20,'rot',-360);

set(gca,'FontSize',FontSize);

% Set ylim

ylimU=max([out.sigma21HPD(:,5); s02]);

ylimL=min([out.sigma21HPD(:,4); s02]);

ylim([ylimL ylimU])

% Set xlim

xlim([xlimL xlimU]);

xL = get(my_subplot,'XLim');

% Add the horizontal line which corresponds to prior value of $\sigma^2$

line(xL,[s02 s02],'Color','r','LineWidth',lwd);

% Add vertical line in correspondence of the step prior to the

% entry of the first outlier

line([dout; dout],[ylimL; ylimU],'Color','r','LineWidth',lwd);

xlabel('Subset size m','FontSize',FontSize);

% Add multiple title

suplabel(['Housing data; forward plots in the interval ['...

num2str(xlimL) ',' num2str(xlimU) ...

'] of HPD regions for \beta and \sigma^2'],'t');

Observed curve of r_min is at least 10 times greater than 99.99% envelope

--------------------------------------------------

-------------------------

Signal detection loop

Tentative signal in central part of the search: step m=511 because

rmin(511,546)>99.99% and rmin(510,546)>99.99% and rmin(512,546)>99.99%

rmin(511,546)>99.999%

-------------------

Signal validation exceedance of upper envelopes

Validated signal

-------------------------------

Start resuperimposing envelopes from step m=510

Superimposition stopped because r_{min}(512,529)>99.9% envelope

Subsample of 528 units is homogeneous

----------------------------

Final output

Number of units declared as outliers=18

Summary of the exceedances

1 99 999 9999 99999

10 64 48 38 29

m=100

m=200

m=300

m=400

m=500

Input Arguments

Output Arguments

References

Chaloner, K. and Brant, R. (1988), A Bayesian Approach to Outlier Detection and Residual Analysis, "Biometrika", Vol. 75, pp. 651-659.

Riani, M., Corbellini, A. and Atkinson, A.C. (2018), Very Robust Bayesian Regression for Fraud Detection, "International Statistical Review", http://dx.doi.org/10.1111/insr.12247

Atkinson, A.C., Corbellini, A. and Riani, M., (2017), Robust Bayesian Regression with the Forward Search: Theory and Data Analysis, "Test", Vol. 26, pp. 869-886, https://doi.org/10.1007/s11749-017-0542-6

|

|

FSRBbsb |

FSRBmdr |

|

|

|

Functions |

|

• The developers of the toolbox • The forward search group • Terms of Use • Acknowledgments