Response variable, specified as

a vector of length n, where n is the number of

observations. Each entry in y is the response for the

corresponding row of X.

Missing values (NaN's) and infinite values (Inf's) are

allowed, since observations (rows) with missing or infinite

values will automatically be excluded from the

computations.

Data Types: single| double

Matrix of explanatory

variables (also called 'regressors') of dimension n x (p-1)

where p denotes the number of explanatory variables

including the intercept.

Rows of X represent observations, and columns represent

variables. By default, there is a constant term in the

model, unless you explicitly remove it using input option

intercept, so do not include a column of 1s in X. Missing

values (NaN's) and infinite values (Inf's) are allowed,

since observations (rows) with missing or infinite values

will automatically be excluded from the computations.

Data Types: single| double

Specify optional comma-separated pairs of Name,Value arguments.

Name is the argument name and Value

is the corresponding value. Name must appear

inside single quotes (' ').

You can specify several name and value pair arguments in any order as

Name1,Value1,...,NameN,ValueN.

Example:

'alpha',0.01

, 'R2th',0.95

, 'fullreweight',true

, 'plotsPI',1

, 'intercept',false

, bayes=struct;bayes.R=R;bayes.n0=n0;bayes.beta0=beta0;bayes.tau0=tau0;

, 'plots',1

, 'tag',{'plmdr' 'plyXplot'};

, 'init',100 starts monitoring from step m=100

, 'nocheck',true

, 'bivarfit',2

, 'multivarfit','1'

, 'labeladd','1'

, 'nameX',{'NameVar1','NameVar2'}

, 'namey','NameOfResponse'

, 'bonflev',0.99

, 'msg',1

Number between 0 and 1 which

defines test size to declare the outliers

Example: 'alpha',0.01

Data Types: double

Scalar which defines the value R2 does

have to exceed. For example, if R2 based on good observations

is 0.92 and R2th is 0.90 the estimate of the variance of the

residuals which is used to declare the outliers is adjusted

in order to have a value of R2 which is equal to 0.90.

Example: 'R2th',0.95

Data Types: double

If fullreweight is true

(default option), the list of outliers refers to all the

units whose residuals is above the threshold else if it is

false the outliers are the observations which by procedure

FSR had been declared outliers and have a residual greater

than threshold

Example: 'fullreweight',true

Data Types: boolean

If plotsPI =1 and

the number of regressors (excluding the constant term) is

equal 1, it is possible to see on the screen the yX scatter

with superimposed the prediction intervals using a

confidence level 1-alpha, else no plot is shown on the

screen

Example: 'plotsPI',1

Data Types: double

Indicator for the constant term (intercept) in the fit,

specified as the comma-separated pair consisting of

'Intercept' and either true to include or false to remove

the constant term from the model.

Example: 'intercept',false

Data Types: boolean

It contains the following fields

| Value |

Description |

beta0 |

p-times-1 vector containing prior mean of \beta

|

R |

p-times-p positive definite matrix which can be

interpreted as X0'X0 where X0 is a n0 x p matrix

coming from previous experiments (assuming that the

intercept is included in the model).

The prior distribution of is a gamma distribution with

parameters a_0 and b_0, that is

p(\tau_0) \propto \tau^{a_0-1} \exp (-b_0 \tau)

\qquad E(\tau_0) = a_0/b_0

|

tau0 |

scalar. Prior estimate of

\tau=1/ \sigma^2 =a_0/b_0

|

n0 |

scalar. Sometimes it helps to think of the prior

information as coming from n0 previous experiments.

Therefore we assume that matrix X0 (which defines

R), was made up of n0 observations.

REMARK if structure bayes is not supplied the default

values which are used are.

beta0= zeros(p,1): Vector of zeros.

R=eye(p): Identity matrix.

tau0=1/1e+6: Very large value for the

prior variance, that is a very

small value for tau0.

n0=1: just one prior observation.

\beta is assumed to have a normal distribution with

mean \beta_0 and (conditional on \tau_0) covariance

(1/\tau_0) (X_0'X_0)^{-1}.

\beta \sim N( \beta_0, (1/\tau_0) (X_0'X_0)^{-1} )

|

Example: bayes=struct;bayes.R=R;bayes.n0=n0;bayes.beta0=beta0;bayes.tau0=tau0;

Data Types: double

If plots=1 (default) the plot of minimum deletion

residual with envelopes based on n observations and the

scatterplot matrix with the outliers highlighted is

produced.

If plots=2 the user can also monitor the intermediate

plots based on envelope superimposition.

Else no plot is produced.

Example: 'plots',1

Data Types: double

This option enables to add a tag to the plots which are

created. The default tag names are:

fsr_mdrplot for the plot of mdr based on all the

observations;

fsr_yXplot for the plot of y against each column of X

with the outliers highlighted;

fsr_resuperplot for the plot of resuperimposed envelopes. The

first plot with 4 panel of resuperimposed envelopes has

tag fsr_resuperplot1, the second fsr_resuperplot2 ...

If tag is character or a cell of characters of length 1,

it is possible to specify the tag for the plot of mdr

based on all the observations;

If tag is a cell of length 2 it is possible to control

both the tag for the plot of mdr based on all the

observations and the tag for the yXplot with outliers

highlighted.

If tag is a cell of length 3 the third element specifies

the names of the plots of resuperimposed envelopes.

Example: 'tag',{'plmdr' 'plyXplot'};

Data Types: char or cell

scalar which specifies the initial subset size to start

monitoring exceedances of minimum deletion residual, if

init is not specified it set equal to:

p+1, if the sample size is smaller than 40;

min(3*p+1,floor(0.5*(n+p+1))), otherwise.

Example: 'init',100 starts monitoring from step m=100

Data Types: double

If nocheck is equal to 1 no check is performed on

matrix y and matrix X. Notice that y and X are left

unchanged. In other words, the additional column of ones

for the intercept is not added. As default nocheck=0.

Example: 'nocheck',true

Data Types: boolean

This option adds one or more least square lines, based on

SIMPLE REGRESSION of y on Xi, to the plots of y|Xi.

bivarfit = ''

is the default: no line is fitted.

bivarfit = '1'

fits a single ols line to all points of each bivariate

plot in the scatter matrix y|X.

bivarfit = '2'

fits two ols lines: one to all points and another to

the group of the genuine observations. The group of the

potential outliers is not fitted.

bivarfit = '0'

fits one ols line to each group. This is useful for the

purpose of fitting mixtures of regression lines.

bivarfit = 'i1' or 'i2' or 'i3' etc.

fits an ols line to a specific group, the one with

index 'i' equal to 1, 2, 3 etc. Again, useful in case

of mixtures.

Example: 'bivarfit',2

Data Types: char

This option adds one or more least square lines, based on

MULTIVARIATE REGRESSION of y on X, to the plots of y|Xi.

multivarfit = ''

is the default: no line is fitted.

multivarfit = '1'

fits a single ols line to all points of each bivariate

plot in the scatter matrix y|X. The line added to the

scatter plot y|Xi is avconst + Ci*Xi, where Ci is the

coefficient of Xi in the multivariate regression and

avconst is the effect of all the other explanatory

variables different from Xi evaluated at their centroid

(that is overline{y}'C))

multivarfit = '2'

equal to multivarfit ='1' but this time we also add the

line based on the group of unselected observations

(i.e. the normal units).

Example: 'multivarfit','1'

Data Types: char

If this option is '1', we label the outliers with the

unit row index in matrices X and y. The default value is

labeladd='', i.e. no label is added.

Example: 'labeladd','1'

Data Types: char

cell array of strings of length p containing the labels of

the variables of the regression dataset. If it is empty

(default) the sequence X1, ..., Xp will be created

automatically

Example: 'nameX',{'NameVar1','NameVar2'}

Data Types: cell

character containing the label of the response

Example: 'namey','NameOfResponse'

Data Types: char

vector with two elements controlling minimum and maximum

on the y axis. Default value is '' (automatic scale)

Example: 'ylim','[0,10]' sets the minimum value to 0 and the

max to 10 on the y axis

Data Types: double

vector with two elements controlling minimum and maximum

on the x axis. Default value is '' (automatic scale)

Example: 'xlim','[0,10]' sets the minimum value to 0 and the

max to 10 on the x axis

Data Types: double

option to be used if the distribution of the data is

strongly non normal and, thus, the general signal

detection rule based on consecutive exceedances cannot be

used. In this case bonflev can be:

- a scalar smaller than 1 which specifies the confidence

level for a signal and a stopping rule based on the

comparison of the minimum MD with a

Bonferroni bound. For example, if bonflev=0.99 the

procedure stops when the trajectory exceeds for the

first time the 99% bonferroni bound.

- A scalar value greater than 1. In this case the

procedure stops when the residual trajectory exceeds

for the first time this value.

Default value is '', which means to rely on general rules

based on consecutive exceedances.

Example: 'bonflev',0.99

Data Types: double

scalar which controls whether to display or not messages

on the screen

If msg==1 (default) messages are displayed on the screen about

step in which signal took place and ....

else no message is displayed on the screen

Example: 'msg',1

Data Types: double

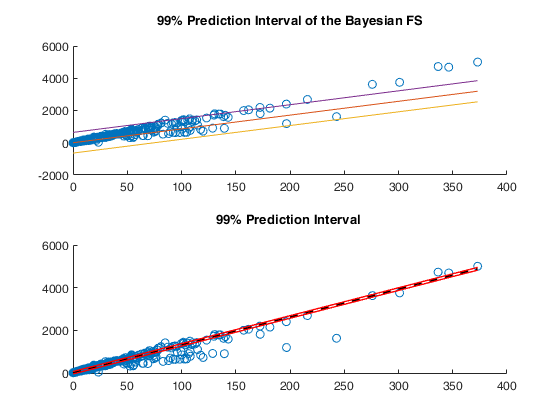

Example of FSRBr for international trade data.

Example of FSRBr for international trade data.