|

LTSts |

LTStsVarSel |

|

LTStsLSmult

LTStsLSmult extends LTSts to the detection of multiple Level Shifts in time series

Description

Examples

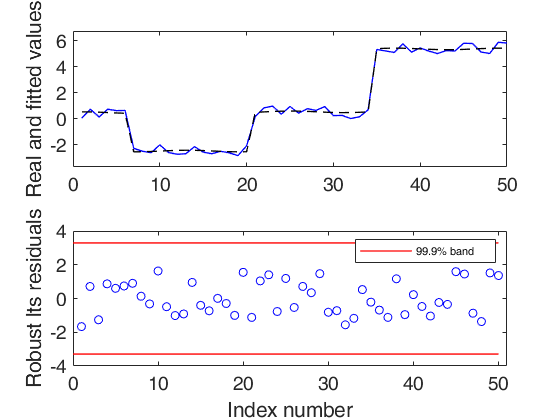

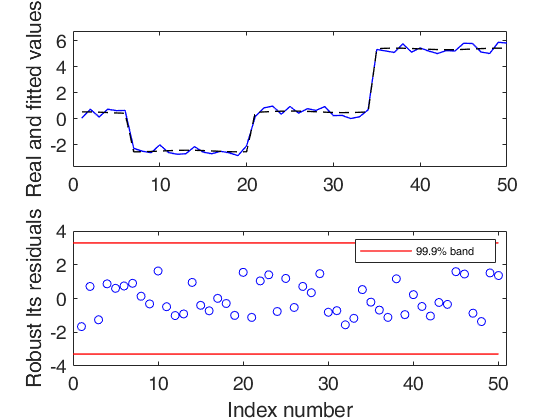

A synthetic example with optional arguments msg and plots.

A synthetic example with optional arguments msg and plots.

A synthetic example with optional arguments msg and plots.

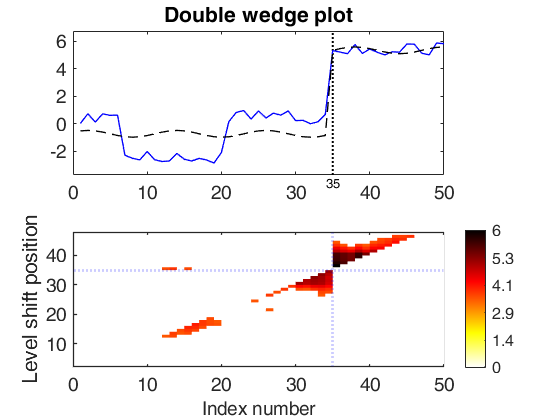

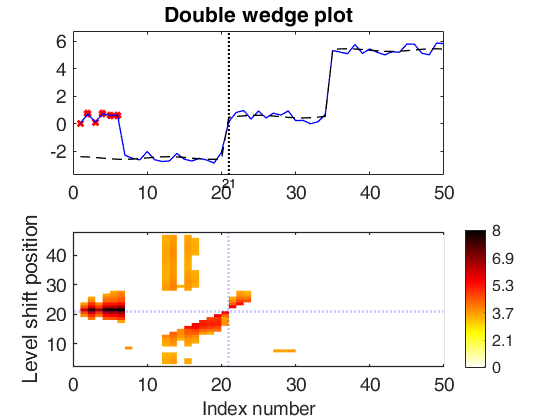

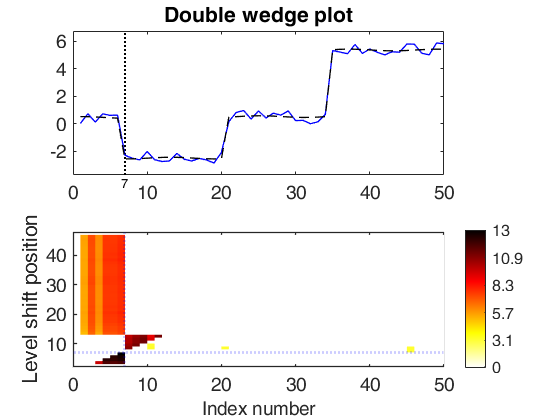

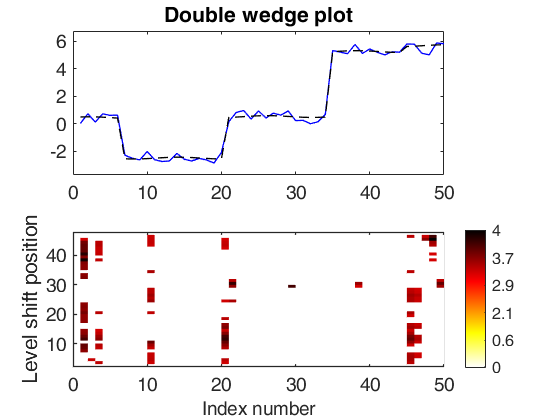

Y=rand(50,1);

Y(35:end)=Y(35:end)+5;

Y(7:20)=Y(7:20)-3;

out = LTStsLSmult(Y,'msg',true,'plots',1);

significant LS at position 35 (pval = 7.1054e-15) significant LS at position 21 (pval = 0) significant LS at position 7 (pval = 0)

Related Examples

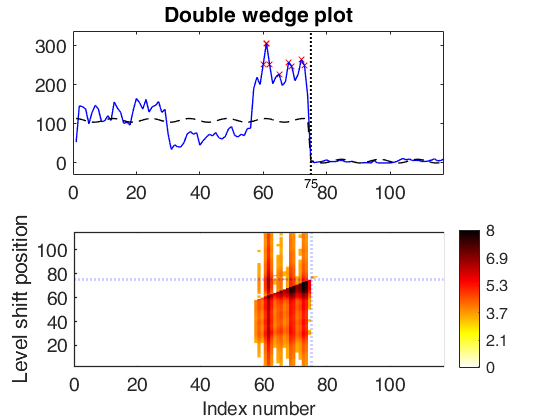

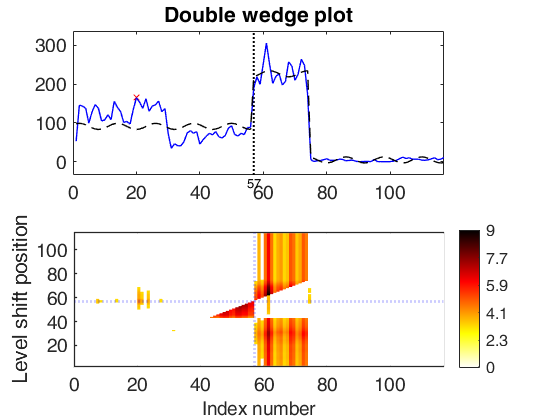

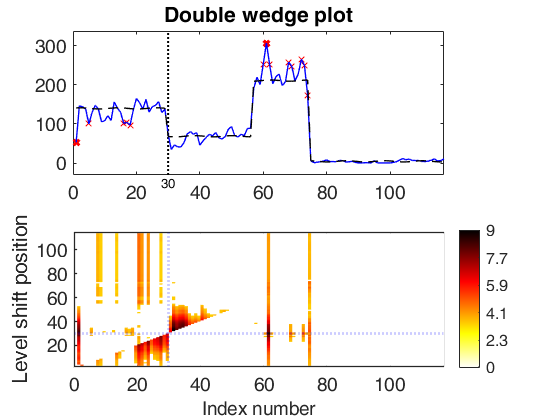

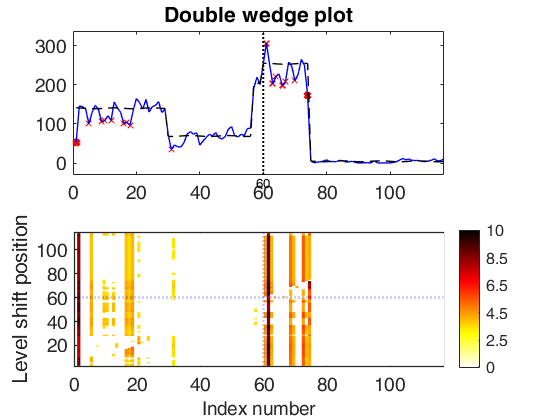

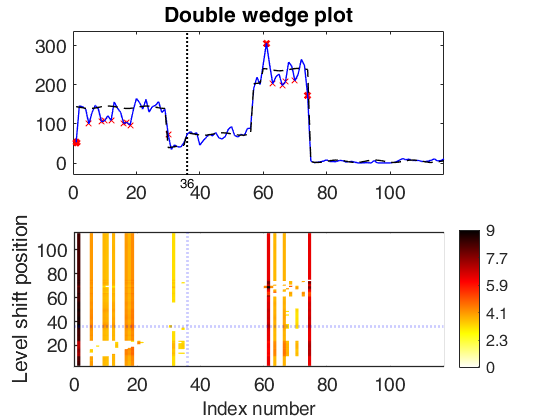

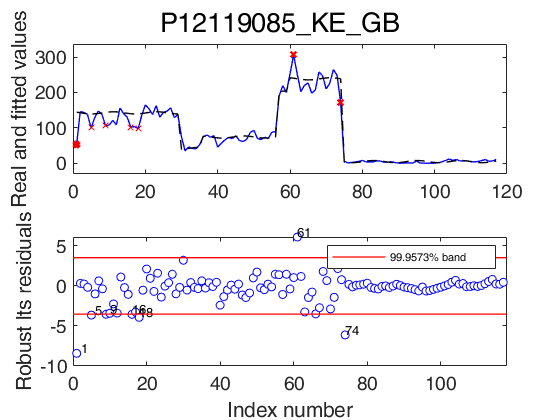

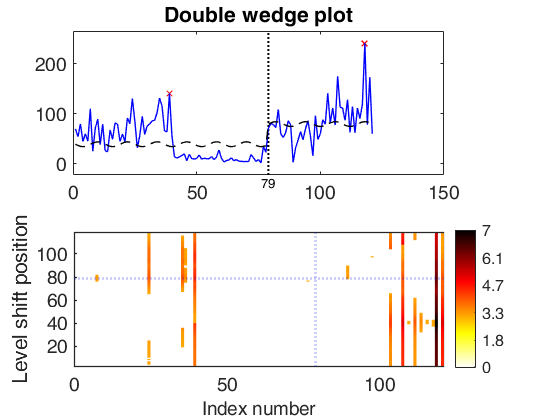

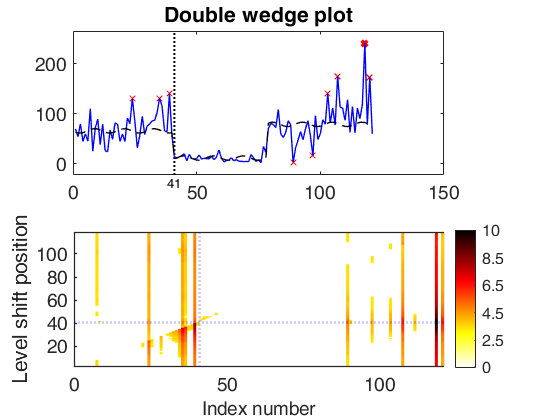

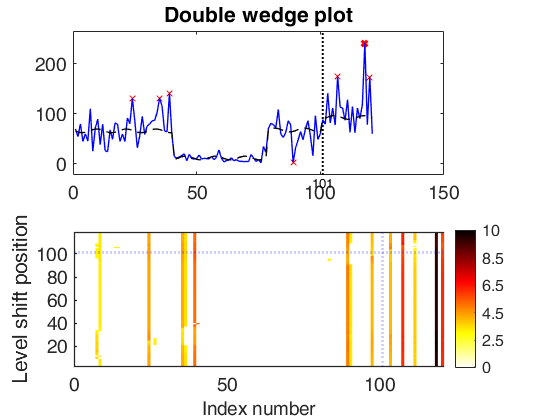

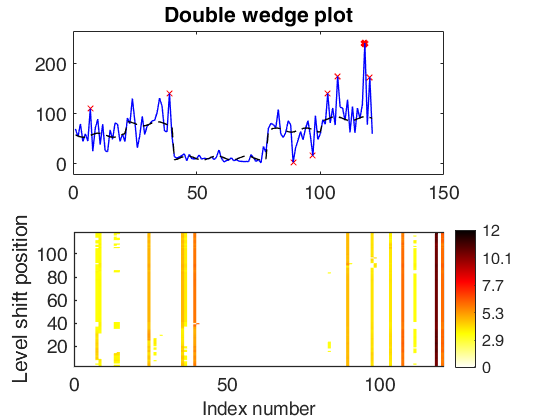

Trade data examples.

Trade data examples.Two examples taken from the (extended version of the) series in: Rousseeuw, P.J., Perrotta D., Riani M. and Hubert, M. (2018), Robust Monitoring of Many Time Series with Application to Fraud Detection, "Econometrics and Statistics".

load TTplant % KE-GB

load TTsugar % UA-LT

yin1 = plant{:,1};

yin2 = sugar{:,1};

out1 = LTStsLSmult(yin1,'msg',true,'plots',1);

sgtitle('P12119085_KE_GB','interpreter','none','Fontsize',20);

pause(1);

out2 = LTStsLSmult(yin2,'msg',true,'plots',1);

sgtitle('P17049075_UA_LT','interpreter','none','Fontsize',20);

significant LS at position 75 (pval = 0) significant LS at position 57 (pval = 0) significant LS at position 30 (pval = 0) significant LS at position 60 (pval = 0) significant LS at position 36 (pval = 1.7337e-10) significant LS at position 79 (pval = 4.793e-06) significant LS at position 41 (pval = 0) significant LS at position 101 (pval = 0.0096827)

Input Arguments

Output Arguments

References

Rousseeuw, P.J., Perrotta D., Riani M. and Hubert, M. (2018), Robust Monitoring of Many Time Series with Application to Fraud Detection, "Econometrics and Statistics". [RPRH]

See Also

|

|

LTSts |

LTStsVarSel |

|

|

|

Functions |

|

• The developers of the toolbox • The forward search group • Terms of Use • Acknowledgments