LTSts

LTSts extends LTS estimator to time series

Description

It is possible to set a model with a trend (up to third order), a seasonality (constant or of varying amplitude and with a different number of harmonics) and a level shift (in this last case it is possible to specify the window in which level shift has to be searched for).

Airline data: linear trend + just one harmonic for seasonal component.out

=LTSts(y,

Name, Value)

Examples

Related Examples

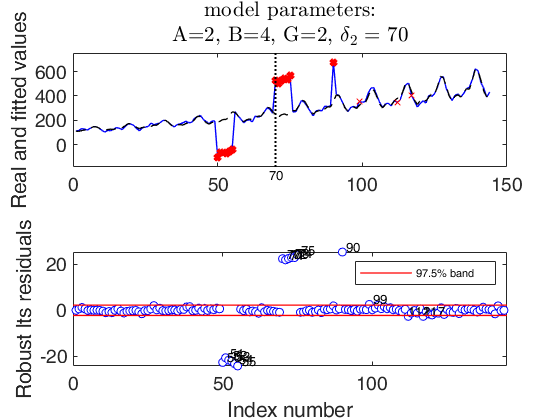

Example 1 used in the paper RPRH.

Example 1 used in the paper RPRH.

Example 1 used in the paper RPRH.Load airline data.

% 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960

y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan

118 126 150 180 196 188 233 277 301 318 342 391 % Feb

132 141 178 193 236 235 267 317 356 362 406 419 % Mar

129 135 163 181 235 227 269 313 348 348 396 461 % Apr

121 125 172 183 229 234 270 318 355 363 420 472 % May

135 149 178 218 243 264 315 374 422 435 472 535 % Jun

148 170 199 230 264 302 364 413 465 491 548 622 % Jul

148 170 199 242 272 293 347 405 467 505 559 606 % Aug

136 158 184 209 237 259 312 355 404 404 463 508 % Sep

119 133 162 191 211 229 274 306 347 359 407 461 % Oct

104 114 146 172 180 203 237 271 305 310 362 390 % Nov

118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec

% Two short level shifts in opposite directions and an isolated outlier.

% Add a level shift contamination plus some outliers.

y1=y(:);

y1(50:55)=y1(50:55)-300;

y1(70:75)=y1(70:75)+300;

y1(90:90)=y1(90:90)+300;

% Create structure specifying model

model=struct;

model.trend=2; % quadratic trend

model.s=12; % monthly time series

model.seasonal=204; % number of harmonics

model.lshift=41:length(y1)-40; % position where monitoring level shift

model.X=[];

% Create structure lts specifying lts options

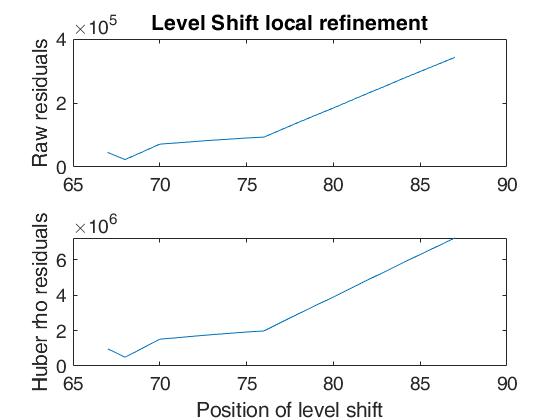

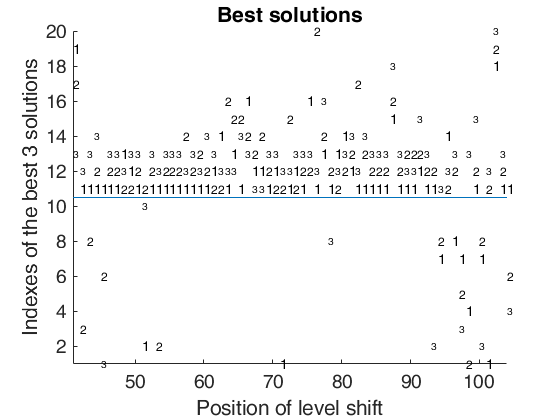

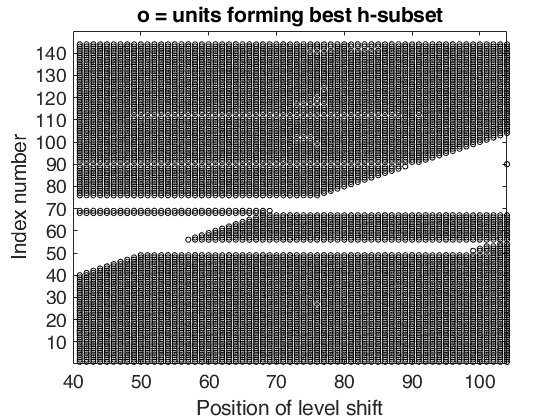

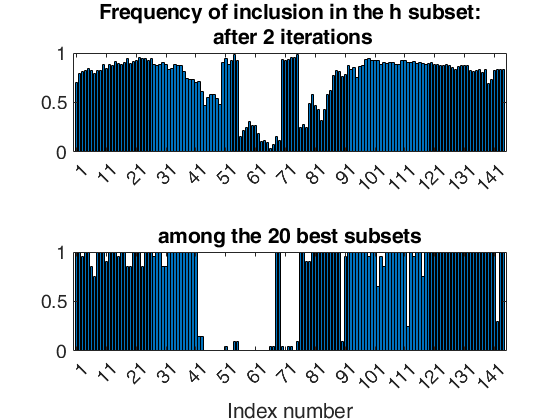

lshiftlocref=struct;

% Set window length for local refinement.

lshiftlocref.wlength=10;

% Set tuning constant to use inside Huber rho function

lshiftlocref.huberc=1.5;

% Estimate the parameters

[out]=LTSts(y1,'model',model,'nsamp',500,...

'plots',1,'lshiftlocref',lshiftlocref,'msg',0);

% Using the notation of the paper RPRH: A=2, B=4, G=2 and $\delta_1>0$.

str=strcat('A=2, B=4, G=2, $\delta_2=',num2str(out.posLS),'$');

numpar = {'model parameters:' , str};

axeslast=findobj('-regexp','Tag','LTSts:ts');

title(axeslast(end),numpar,'interpreter','LaTeX','FontSize',16);

% generate the wedgeplot

% wedgeplot(out,'transpose',true,'extradata',[y1 out.yhat]);

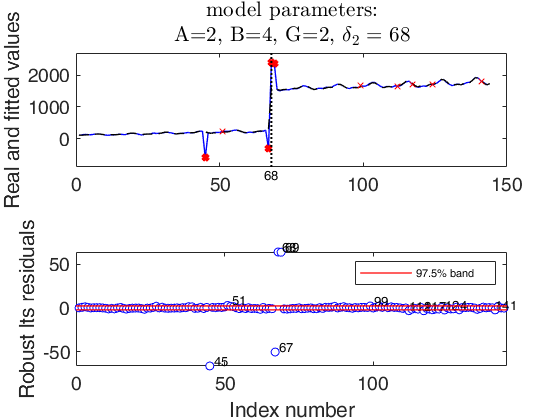

Example 2 used in the paper RPRH.

Example 2 used in the paper RPRH.A persisting level shift and three isolated outliers, two of which in proximity of the level shift.

% Load airline data.

% 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960

y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan

118 126 150 180 196 188 233 277 301 318 342 391 % Feb

132 141 178 193 236 235 267 317 356 362 406 419 % Mar

129 135 163 181 235 227 269 313 348 348 396 461 % Apr

121 125 172 183 229 234 270 318 355 363 420 472 % May

135 149 178 218 243 264 315 374 422 435 472 535 % Jun

148 170 199 230 264 302 364 413 465 491 548 622 % Jul

148 170 199 242 272 293 347 405 467 505 559 606 % Aug

136 158 184 209 237 259 312 355 404 404 463 508 % Sep

119 133 162 191 211 229 274 306 347 359 407 461 % Oct

104 114 146 172 180 203 237 271 305 310 362 390 % Nov

118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec

close all

y1=y(:);

y1(68:end)=y1(68:end)+1300;

y1(67)=y1(67)-600;

y1(45)=y1(45)-800;

y1(68:69)=y1(68:69)+800;

% Create structure specifying model

model=struct;

model.trend=2; % quadratic trend

model.s=12; % monthly time series

model.seasonal=204; % number of harmonics

model.lshift=41:length(y1)-40; % position where monitoring level shift

model.X=[];

% Create structure lts specifying lts options

lshiftlocref=struct;

% Set window length for local refinement.

lshiftlocref.wlength=10;

% Set tuning constant to use inside Huber rho function

lshiftlocref.huberc=1.5;

% Estimate the parameters

[out, varargout]=LTSts(y1,'model',model,'nsamp',500,...

'plots',1,'lshiftlocref',lshiftlocref,'msg',0);

% Using the notation of the paper RPRH: A=2, B=4, G=2 and $\delta_1>0$.

str=strcat('A=2, B=4, G=2, $\delta_2=',num2str(out.posLS),'$');

numpar = {'model parameters:' , str};

title(findobj('-regexp','Tag','LTSts:ts'),numpar,'interpreter','LaTeX','FontSize',16);

% generate the wedgeplot

% wedgeplot(out,'transpose',true,'extradata',[y1 out.yhat]);

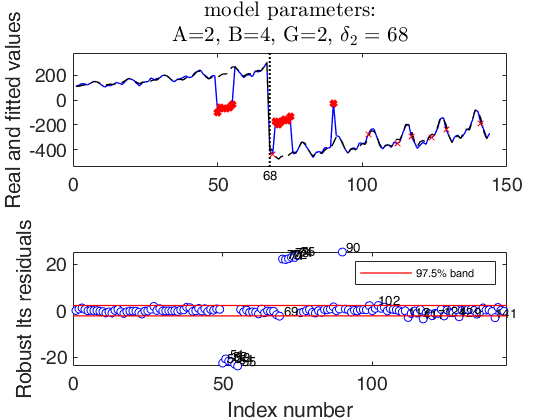

Example 3 used in the paper RPRH.

Example 3 used in the paper RPRH.A persisting level shift preceded and followed in the proximity by other two short level shifts, and an isolated outlier.

% Load airline data.

% 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960

y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan

118 126 150 180 196 188 233 277 301 318 342 391 % Feb

132 141 178 193 236 235 267 317 356 362 406 419 % Mar

129 135 163 181 235 227 269 313 348 348 396 461 % Apr

121 125 172 183 229 234 270 318 355 363 420 472 % May

135 149 178 218 243 264 315 374 422 435 472 535 % Jun

148 170 199 230 264 302 364 413 465 491 548 622 % Jul

148 170 199 242 272 293 347 405 467 505 559 606 % Aug

136 158 184 209 237 259 312 355 404 404 463 508 % Sep

119 133 162 191 211 229 274 306 347 359 407 461 % Oct

104 114 146 172 180 203 237 271 305 310 362 390 % Nov

118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec

y1=y(:);

y1(50:55)=y1(50:55)-300;

y1(68:end)=y1(68:end)-700;

y1(70:75)=y1(70:75)+300;

y1(90:90)=y1(90:90)+300;

% Create structure specifying model

model=struct;

model.trend=2; % quadratic trend

model.s=12; % monthly time series

model.seasonal=204; % number of harmonics

model.lshift=41:length(y1)-40; % position where monitoring level shift

model.X=[];

% Create structure lts specifying lts options

lshiftlocref=struct;

% Set window length for local refinement.

lshiftlocref.wlength=10;

% Set tuning constant to use inside Huber rho function

lshiftlocref.huberc=1.5;

close all

% Estimate the parameters

[out, varargout]=LTSts(y1,'model',model,'nsamp',500,...

'plots',2,'lshiftlocref',lshiftlocref,'msg',0);

% Using the notation of the paper RPRH: A=2, B=4, G=2 and $\delta_1>0$.

str=strcat('A=2, B=4, G=2, $\delta_2=',num2str(out.posLS),'$');

numpar = {'model parameters:' , str};

title(findobj('-regexp','Tag','LTSts:ts'),numpar,'interpreter','LaTeX','FontSize',16);

% generate the wedgeplot

% wedgeplot(out,'transpose',true,'extradata',[y1 out.yhat]);

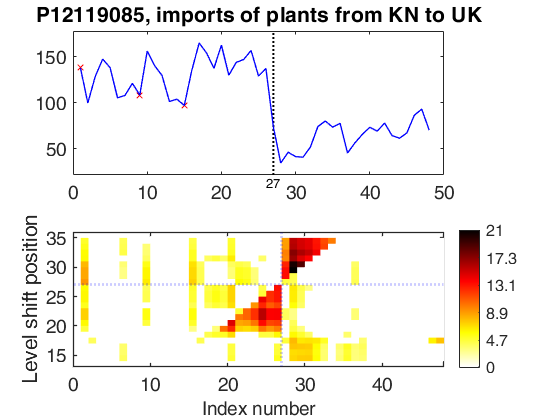

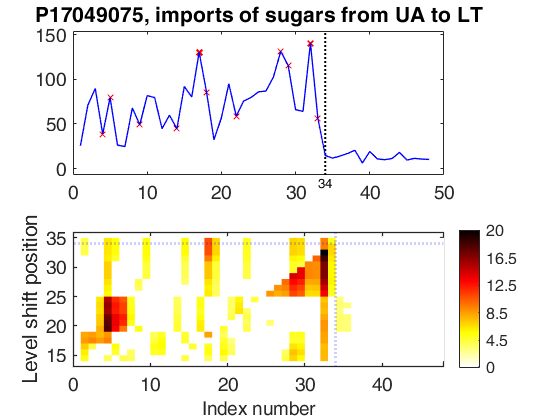

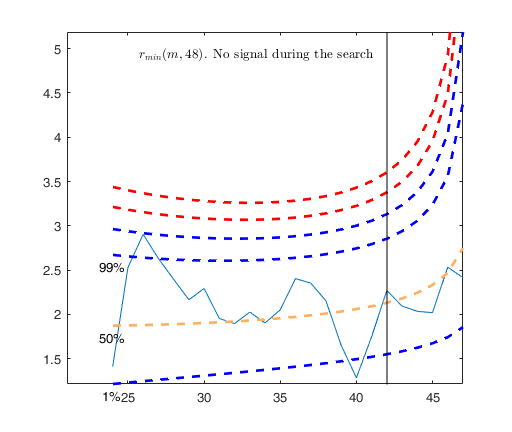

Examples 4 and 5 used in the paper RPRH: trade data.

Examples 4 and 5 used in the paper RPRH: trade data.

%% Examples 4 and 5 used in the paper RPRH: trade data.

close all; clear all;

% the datasets

load('TTP12119085');

load('TTP17049075');

Y4 = P12119085{:,1};

Y5 = P17049075{:,1};

% the model

model = struct;

model.trend = 1;

model.seasonal = 102;

model.s = 12;

model.lshift = 14:length(Y4)-13;

% LTSts

out4 = LTSts(Y4,'model',model,'plots',0,'dispresults',true,'msg',0);

out5 = LTSts(Y5,'model',model,'plots',0,'dispresults',true,'msg',0);

% the wedgeplot with the time series and the detected outliers and

% level shift

wedgeplot(out4,'extradata',Y4,'titl','P12119085, imports of plants from KN to UK');

wedgeplot(out5,'extradata',Y5,'titl','P17049075, imports of sugars from UA to LT');

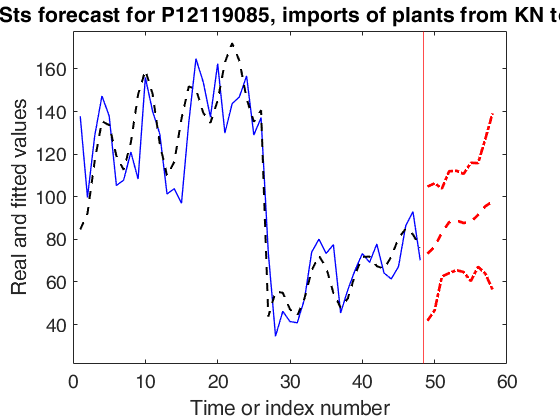

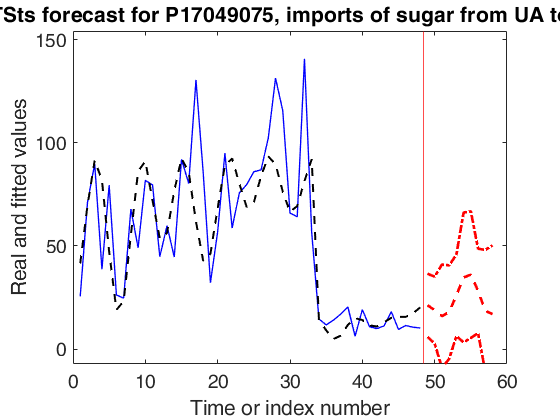

% Forecasts with a 99.9 per cent confidence level

nfore=10;

outfore4 = forecastTS(out4,'model',model,'nfore',nfore,'conflev',0.999,'titl','LTSts forecast for P12119085, imports of plants from KN to UK');

outfore5 = forecastTS(out5,'model',model,'nfore',nfore,'conflev',0.999,'titl','LTSts forecast for P17049075, imports of sugar from UA to LT');

% Comparing with FS (needs conflev option)

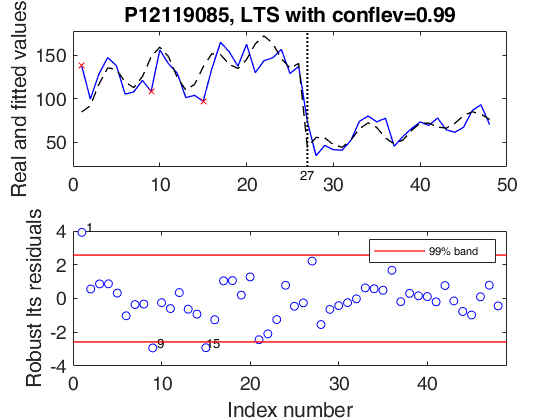

outLTS4 = LTSts(Y4,'model',model,'plots',1,'conflev',0.99,'msg',0);

drawnow;

ax = findall(0, 'Type', 'axes', 'Tag', 'LTSts:ts');

title(ax,'P12119085, LTS with conflev=0.99');

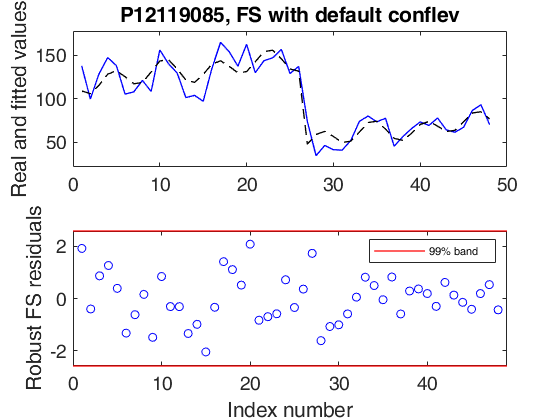

outFRS4 = FSRts(Y4,'model',model,'plots',1);

ax=findobj(gcf,'Tag','FSRts:ts');

title(ax,'P12119085, FS with default conflev');

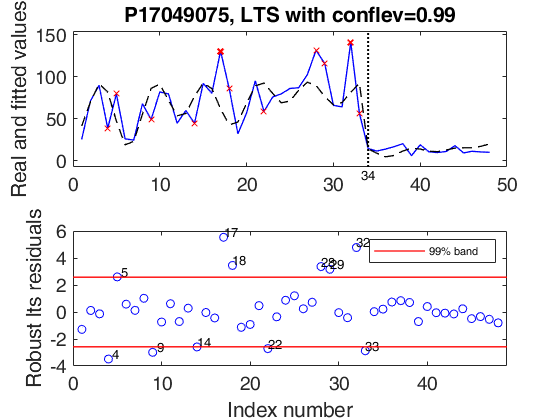

outLTS5 = LTSts(Y5,'model',model,'plots',1,'conflev',0.99,'msg',0);

ax=findobj(gcf,'Tag','LTSts:ts');

title(ax,'P17049075, LTS with conflev=0.99');

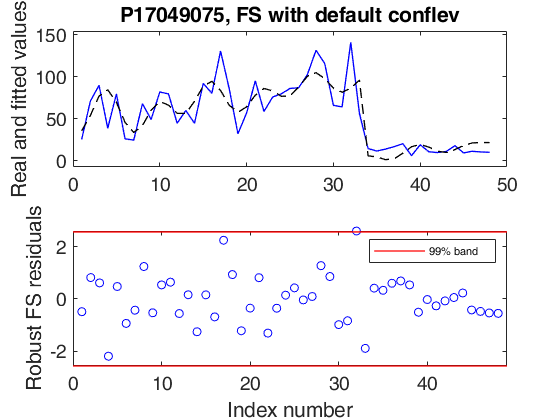

outFRS5 = FSRts(Y5,'model',model,'plots',1);

ax=findobj(gcf,'Tag','FSRts:ts');

title(ax,'P17049075, FS with default conflev'); Coeff SE t pval

_______ ____ ______ ____

b_trend1 115.27 4.51 25.59 0.00

b_trend2 1.59 0.27 5.80 0.00

b_cos1 -2.83 3.92 -0.72 0.47

b_sin1 -12.42 4.69 -2.65 0.01

b_cos2 -9.07 4.66 -1.95 0.06

b_sin2 -22.60 4.71 -4.80 0.00

b_varaml -0.02 0.00 -3.72 0.00

b_lshift -112.62 7.63 -14.76 0.00

Level shift position t=27

Coeff SE t pval

______ ____ ______ ____

b_trend1 55.14 3.85 14.30 0.00

b_trend2 0.90 0.20 4.52 0.00

b_cos1 15.54 4.15 3.75 0.00

b_sin1 3.61 4.27 0.85 0.40

b_cos2 -32.50 4.25 -7.64 0.00

b_sin2 -16.06 4.31 -3.72 0.00

b_varaml -0.02 0.00 -12.15 0.00

b_lshift -79.41 5.70 -13.94 0.00

Level shift position t=34

Level shift for t=14

Level shift for t=15

Level shift for t=16

Level shift for t=17

Level shift for t=18

Level shift for t=19

Level shift for t=20

Level shift for t=21

Level shift for t=22

Level shift for t=23

Level shift for t=24

Level shift for t=25

Level shift for t=26

Level shift for t=27

Level shift for t=28

Level shift for t=29

Level shift for t=30

Level shift for t=31

Level shift for t=32

Level shift for t=33

Level shift for t=34

Level shift for t=35

-------------------------

Signal detection loop

Sample seems homogeneous, no outlier has been found

Summary of the exceedances

1.00 99.00 999.00 9999.00 99999.00

1.00 2.00 0 0 0

Level shift for t=14

Level shift for t=15

Level shift for t=16

Level shift for t=17

Level shift for t=18

Level shift for t=19

Level shift for t=20

Level shift for t=21

Level shift for t=22

Level shift for t=23

Level shift for t=24

Level shift for t=25

Level shift for t=26

Level shift for t=27

Level shift for t=28

Level shift for t=29

Level shift for t=30

Level shift for t=31

Level shift for t=32

Level shift for t=33

Level shift for t=34

Level shift for t=35

-------------------------

Signal detection loop

Sample seems homogeneous, no outlier has been found

Summary of the exceedances

1.00 99.00 999.00 9999.00 99999.00

0 5.00 1.00 0 0

Input Arguments

Output Arguments

References

Rousseeuw, P.J., Perrotta D., Riani M. and Hubert, M. (2018), Robust Monitoring of Many Time Series with Application to Fraud Detection, "Econometrics and Statistics". [RPRH]