regressHhar

regressHhar fits a multiple linear regression model with Harvey heteroskedasticity

Description

Examples

regressHhar with all default options.

regressHhar with all default options.

regressHhar with all default options.Monthly credit card expenditure for 100 individuals.

% Results in structure "OUT" coincides with "Maximum Likelihood

% Estimates" of table 11.3, page 235, 5th edition of Greene (1987).

% Results in structure "OLS" coincide with "Ordinary Least Squares

% Estimates" of table 11.3, page 235, 5th edition of Greene (1987).

load('TableF91_Greene');

data=TableF91_Greene{:,:};

n=size(data,1);

% Linear regression of monthly expenditure on a constant, age, income

% its square and a dummy variable for home ownership using the 72

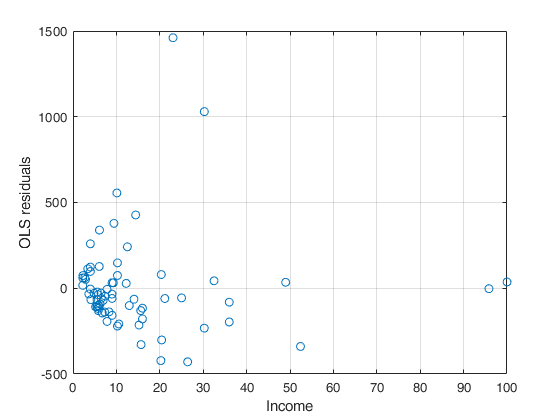

% observations for which expenditure was nonzero produces the residuals

% plotted below.

X=zeros(n,4);

X(:,1)=data(:,3); % age

X(:,2)=data(:,6); % Own rent (dummy variable)

X(:,3)=data(:,4); % Income

X(:,4)=(data(:,4)).^2; % Income square

y=data(:,5); % Monthly expenditure

% Select the 72 observations for which expenditure was nonzero

sel=y>0;

X=X(sel,:);

y=y(sel);

whichstats={'r','tstat'};

OLS=regstats(y,X,'linear',whichstats);

r=OLS.r;

disp('Ordinary Least Squares Estimates')

LSest=[OLS.tstat.beta OLS.tstat.se OLS.tstat.t OLS.tstat.pval];

disp(LSest)

disp('Multiplicative Heteroskedasticity Model')

% The variables which enter the scedastic function are Income and

% Income square (that is columns 3 and 4 of matrix X).

out=regressHhar(y,X,[3 4]);

% Plot OLS residuals against Income (This is nothing but Figure 11.1 of

% Green (5th edition) p. 216).

plot(X(:,4),r,'o')

xlabel('Income')

ylabel('OLS residuals')

grid on

Ordinary Least Squares Estimates -237.1465 199.3517 -1.1896 0.2384 -3.0818 5.5147 -0.5588 0.5781 27.9409 82.9223 0.3370 0.7372 234.3470 80.3660 2.9160 0.0048 -14.9968 7.4693 -2.0078 0.0487 Multiplicative Heteroskedasticity Model

Related Examples

FGLS estimator.

FGLS estimator.Estimate a multiplicative heteroscedastic model using just one iteration that is find FGLS estimator (two step estimator).

% Data are monthly credit card expenditure for 100 individuals.

% Results in structure "out" coincide with estimates of row

% "$\sigma^2_i=\sigma^2 \exp(z' \alpha)$" in table 11.2, page 231, 5th edition of

% Greene (1987).

load('TableF91_Greene');

data=TableF91_Greene{:,:};

n=size(data,1);

% Linear regression of monthly expenditure on a constant, age, income and

% its square and a dummy variable for home ownership using the 72

% observations for which expenditure was nonzero produces the residuals

% plotted below.

X=zeros(n,4);

X(:,1)=data(:,3); % age

X(:,2)=data(:,6); % Own rent (dummy variable)

X(:,3)=data(:,4); % Income

X(:,4)=(data(:,4)).^2; % Income square

y=data(:,5); % Monthly expenditure

% Select the 72 observations for which expenditure was nonzero

sel=y>0;

X=X(sel,:);

y=y(sel);

out=regressHhar(y,X,[3 4],'msgiter',1,'maxiter',1);

Regression parameters beta

Coeff. SE t-stat

-117.8675 50.4970 -2.3341

-1.2337 1.2707 -0.9709

50.9498 26.3050 1.9369

145.3045 23.0917 6.2925

-7.9383 1.8611 -4.2653

Scedastic parameters gamma from first iteration

Coeff.

4.1374

2.4857

-0.2449

Input Arguments

Output Arguments

More About

References

Greene W.H. (1987), Econometric Analysis, Prentice Hall. [5th edition, section 11.7.1 pp. 232-235, 7th edition, section 9.7.1 pp. 280-282].