VIOM

VIOM computes weights estimates under Variance-Inflation Model

Description

Examples

VIOM with default input.

VIOM with default input.

VIOM with default input.

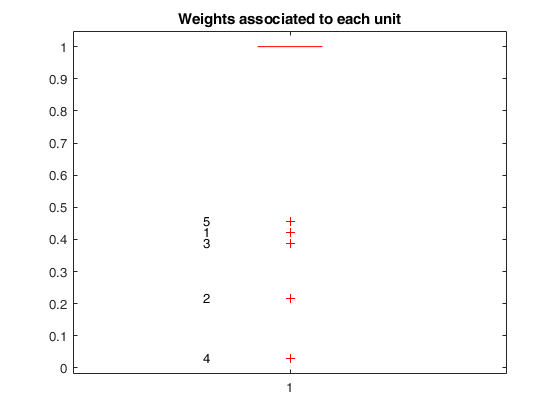

n=200;

p=3;

randn('state', 123456);

X=randn(n,p);

y=randn(n,1);

y(1:5)=y(1:5)*2;

[out]=VIOM(y,X, 1:5);

% Show the weights associated to each unit.

figure

boxplot(out.w)

out.w(1:5);

for i=1:n

if out.w(i)<0.9

text(0.8,out.w(i),num2str(i))

end

end

title('Weights associated to each unit')

out.beta;

Related Examples

Input Arguments

Output Arguments

References

Cook, R.D., Holschuh N., and Weisberg S. (1982). A note on an alternative outlier model, "Journal of the Royal Statistical Society:

Series B (Methodological)", Vol. 44, pp. 370-376.

Thompson, R. (1985), A note on restricted maximum likelihood estimation with an alternative outlier model, "Journal of the Royal Statistical Society: Series B (Methodological)", Vol. 47, pp. 53-55.

Gumedze, F.N. (2019), Use of likelihood ratio tests to detect outliers under the variance shift outlier model, "Journal of Applied Statistics", Vol. 46, pp. 598-620.