forecastH

forecastH produce forecasts with confidence bands for regression model with heteroskedasticity

Description

Examples

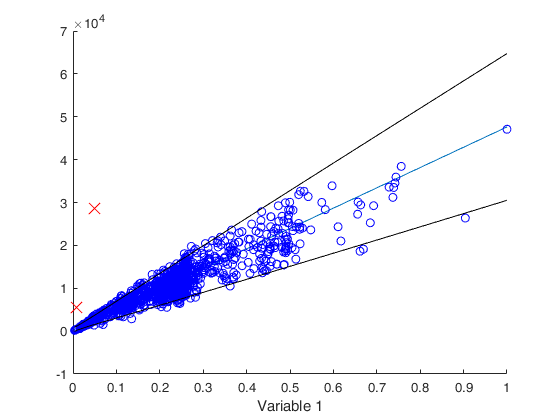

Example of use of option bsb.

Example of use of option bsb.

Example of use of option bsb.

close all

load tradeH.mat

y=tradeH{:,2};

X=tradeH{:,1};

X=X./max(X);

Z=log(X);

n=length(y);

bsb=1:n;

% outl = the outliers

outl=[225 660];

bsb(outl)=[];

% call of forecastH with option bsb

outFORE=forecastH(y,X,Z,'bsb',bsb);

Related Examples

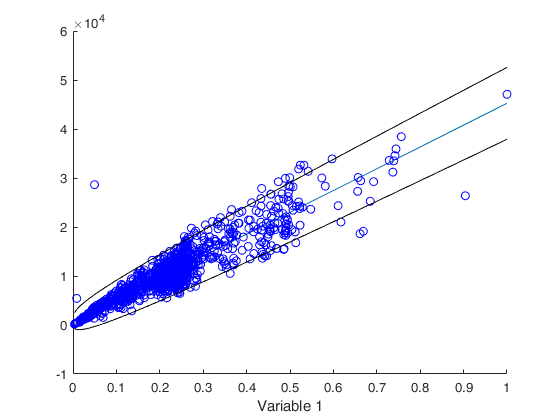

Example of use of option typeH.

Example of use of option typeH.

close all

load tradeH.mat

y=tradeH{:,2};

X=tradeH{:,1};

X=X./max(X);

Z=log(X);

% Use Harvery's parametrization

fore=forecastH(y,X,Z,'typeH','har');

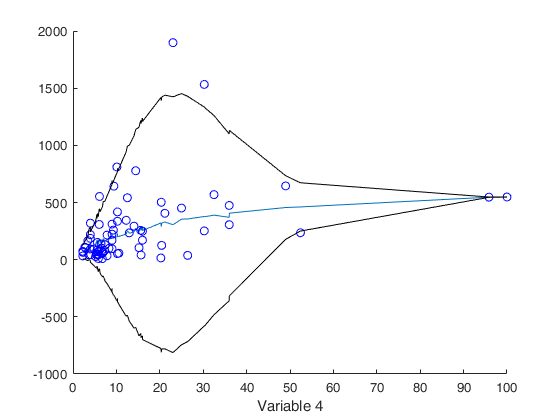

Monthly credit card expenditure for 100 individuals.

Monthly credit card expenditure for 100 individuals.Example of use of option selcolX

load('TableF91_Greene');

data=TableF91_Greene{:,:};

n=size(data,1);

% Linear regression of monthly expenditure on a constant, age, income

% its square and a dummy variable for home ownership using the 72

% observations for which expenditure was nonzero produces the residuals

% plotted below

X=zeros(n,4);

X(:,1)=data(:,3);%age

X(:,2)=data(:,6);% Own rent (dummy variable)

X(:,3)=data(:,4);% Income

X(:,4)=(data(:,4)).^2; %Income square

y=data(:,5); % Monthly expenditure

% Select the 72 observations for which expenditure was nonzero

sel=y>0;

X=X(sel,:);

y=y(sel);

close all

disp('Multiplicative Heteroskedasticity Model')

% Plot of forecasts against column 4

warning('off')

out=forecastH(y,X,[3 4],'typeH','har','selcolX',4);

warning('on')Multiplicative Heteroskedasticity Model

Input Arguments

Output Arguments

References

Greene, W.H. (1987), "Econometric Analysis", Prentice Hall. [5th edition, section 11.7.1 pp. 232-235, 7th edition, section 9.7.1 pp. 280-282]

Atkinson, A.C., Riani, M. and Torti, F. (2016), Robust methods for heteroskedastic regression, "Computational Statistics and Data Analysis", Vol. 104, pp. 209-222, http://dx.doi.org/10.1016/j.csda.2016.07.002 [ART]