forecastTS

Forecast for a time series with trend, time varying seasonal, level shift and irregular component

Description

forecastTS produces forecasts with confidence bands for a time series with trend (up to third order), seasonality (constant or of varying amplitude) with a different number of harmonics, level shift and explanatory variables.

Quadratic trend and constant seasonal.outFORE

=forecastTS(outEST,

Name, Value)

Examples

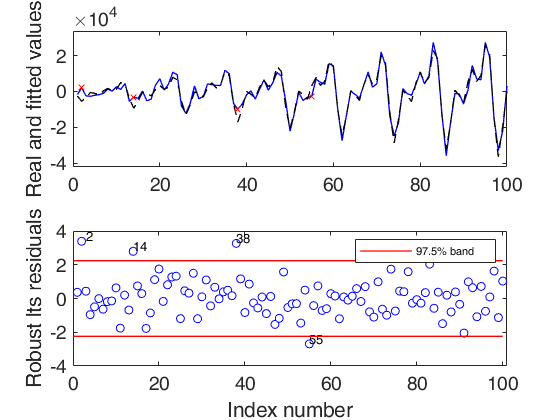

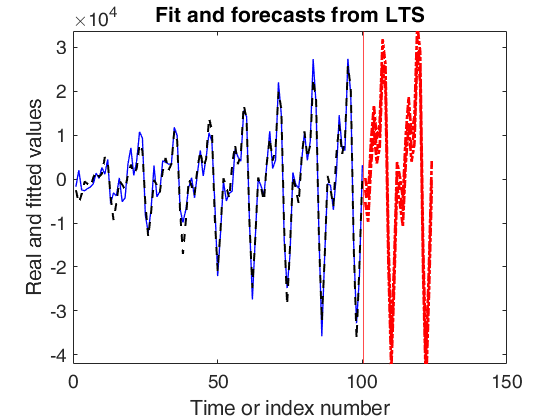

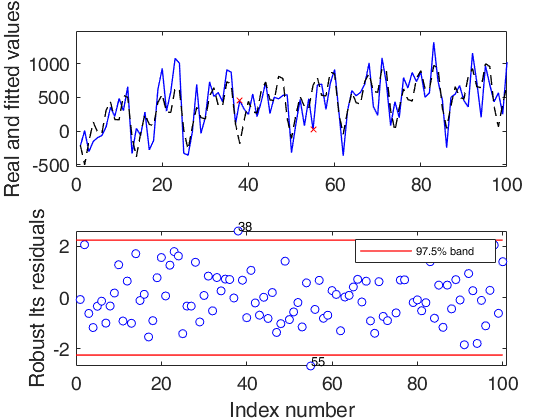

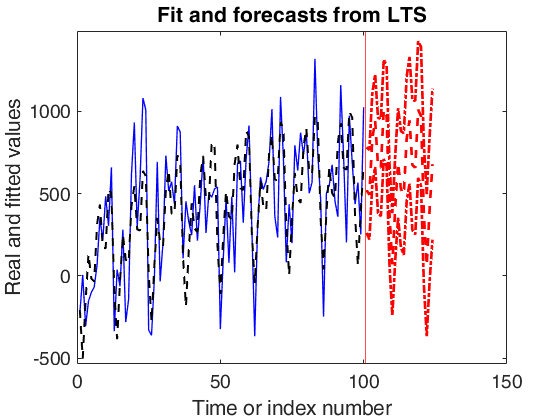

Linear time varying seasonal component.

Linear time varying seasonal component.

Linear time varying seasonal component.

close all

rng('default')

rng(1)

model=struct;

model.trend=1;

model.seasonal=103;

modelSIM=model;

modelSIM.trendb=[0 0];

modelSIM.seasonalb=40*[0.1 -0.5 0.2 -0.3 0.3 -0.1 0.222];

modelSIM.signal2noiseratio=20;

T=100;

% Simulate

outSIM=simulateTS(T,'model',modelSIM,'plots',1);

ySIM=outSIM.y;

% Estimate

outEST=LTSts(ySIM,'model',model,'plots',1);

% Forecast

outFORE=forecastTS(outEST,'model',model,'plots',1);

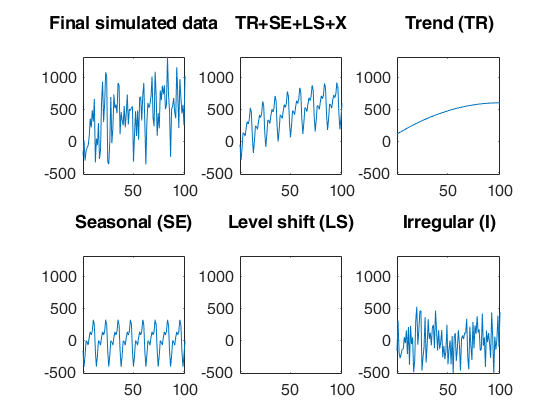

Quadratic trend and constant seasonal.

Quadratic trend and constant seasonal.

close all rng(1) model=struct; model.trend=2; model.seasonal=3; modelSIM=model; modelSIM.trendb=[100 10 -0.05]; modelSIM.seasonalb=400*[0.1 -0.5 0.2 -0.3 0.3 -0.1]; modelSIM.signal2noiseratio=1; T=100; % Simulate outSIM=simulateTS(T,'model',modelSIM,'plots',1); ySIM=outSIM.y; % Estimate outEST=LTSts(ySIM,'model',model,'plots',1); % Forecast outFORE=forecastTS(outEST,'model',model,'plots',1);

Related Examples

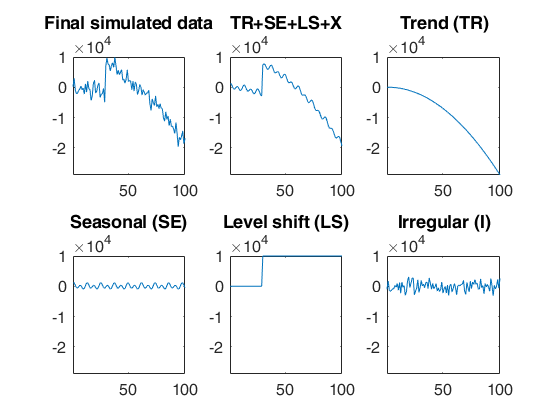

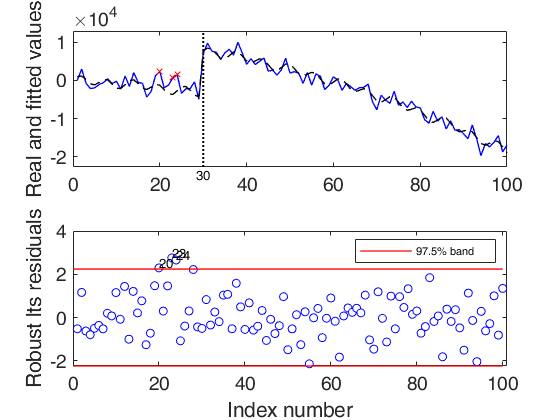

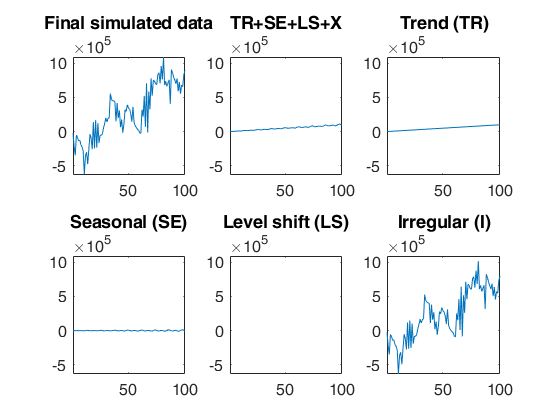

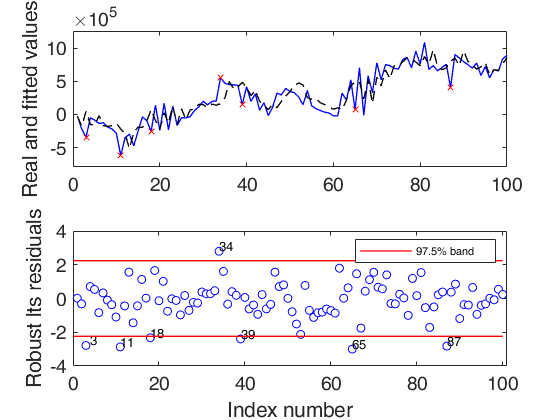

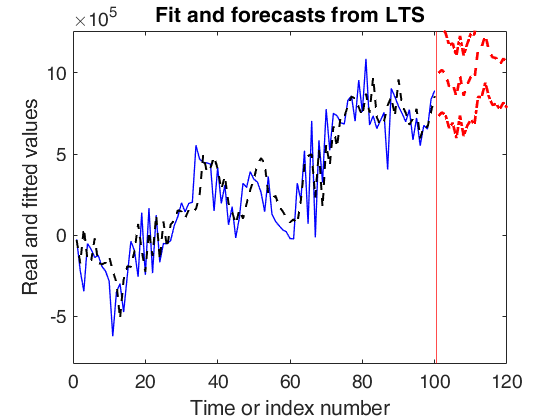

Simulated time series with quadratic trend, fixed seasonal and level shift.

Simulated time series with quadratic trend, fixed seasonal and level shift.A time series of 100 observations is simulated from a model which contains a quadratic trend, a seasonal component with two harmonics no explanatory variables and a level shift in position 30 with size 5000 and a signal to noise ratio equal to 20

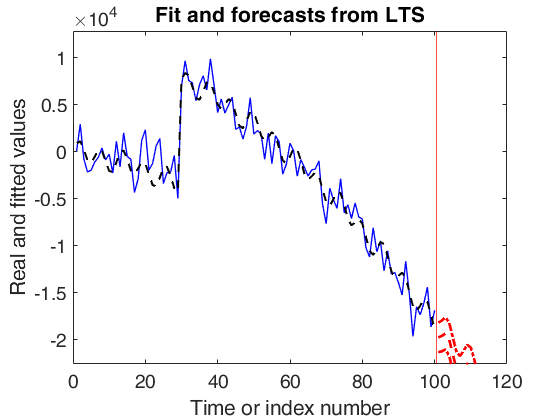

close all rng(1) model=struct; model.trend=2; model.seasonal=2; model.lshift=30; modelSIM=model; modelSIM.trendb=[5,10,-3]; modelSIM.seasonalb=100*[2 4 0.1 8]; modelSIM.signal2noiseratio=20; modelSIM.lshiftb=10000; T=100; % Simulate outSIM=simulateTS(T,'model',modelSIM,'plots',1); ySIM=outSIM.y; % Estimate % model.lshift=5:T-5 implies that LS is investigated from position % $5, 6, 7, ..., T-5$, model.lshift=5:T-5; outEST=LTSts(ySIM,'model',model,'plots',1,'msg',0); % Forecast outFORE=forecastTS(outEST,'model',model,'plots',1);

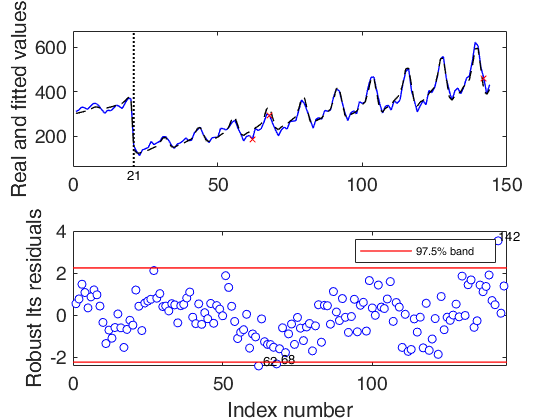

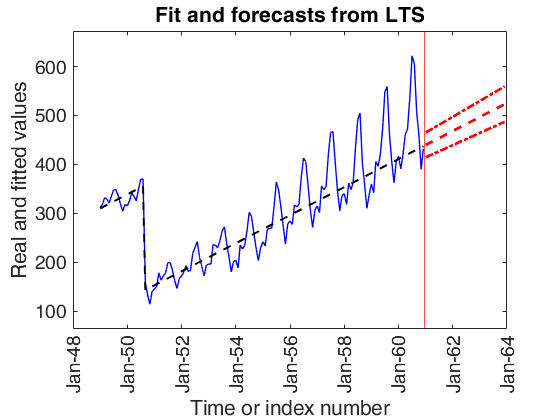

Contaminated airline data (1).

Contaminated airline data (1).Load the data.

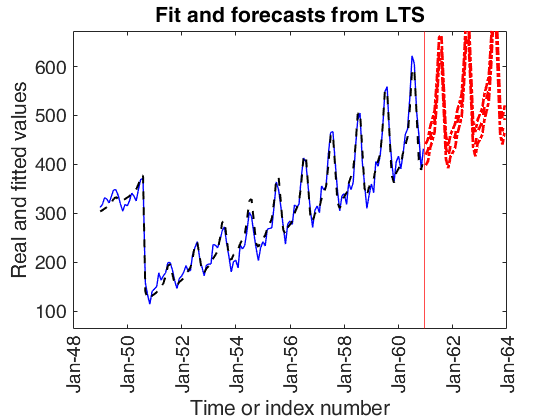

% 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960 y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan 118 126 150 180 196 188 233 277 301 318 342 391 % Feb 132 141 178 193 236 235 267 317 356 362 406 419 % Mar 129 135 163 181 235 227 269 313 348 348 396 461 % Apr 121 125 172 183 229 234 270 318 355 363 420 472 % May 135 149 178 218 243 264 315 374 422 435 472 535 % Jun 148 170 199 230 264 302 364 413 465 491 548 622 % Jul 148 170 199 242 272 293 347 405 467 505 559 606 % Aug 136 158 184 209 237 259 312 355 404 404 463 508 % Sep 119 133 162 191 211 229 274 306 347 359 407 461 % Oct 104 114 146 172 180 203 237 271 305 310 362 390 % Nov 118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec y=y(:); % Contaminate the first 20 observations y(1:20)=y(1:20)+200; close all % Model with linear trend, three harmonics for seasonal component and % varying amplitude using a linear trend. Search for a level shift model=struct; model.trend=1; % linear trend model.s=12; % monthly time series model.seasonal=103; % three harmonics with linear time varying seasonality model.lshift=10:140; % search for level shift out=LTSts(y,'model',model,'plots',1,'dispresults',true,'msg',0); % 3 years forecasts nfore=36; StartDate=[1949 1]; conflev=0.999; % Wide confidence level for the forecast outFORE=forecastTS(out,'model',model,'nfore',nfore,'StartDate',StartDate,'conflev',conflev);

Coeff SE t pval

_________ _______ ________ ___________

b_trend1 301.9 3.3707 89.565 1.9432e-121

b_trend2 2.7697 0.03804 72.811 1.2536e-109

b_cos1 -0.94446 2.822 -0.33468 0.73839

b_sin1 -0.46559 1.3917 -0.33454 0.7385

b_cos2 -0.036471 0.11546 -0.31586 0.7526

b_sin2 0.55656 1.6636 0.33455 0.73849

b_cos3 0.22205 0.66425 0.33428 0.73869

b_sin3 -0.093486 0.28116 -0.3325 0.74003

b_varaml 0.58107 1.7666 0.32891 0.74273

b_lshift -225.91 4.5415 -49.743 2.9417e-88

Level shift position t=21

Contaminated airline data (2).

Contaminated airline data (2).

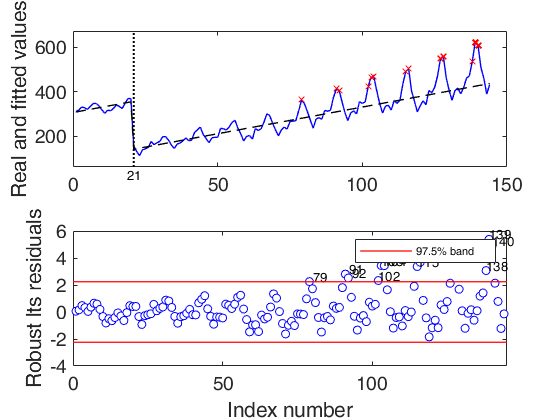

close all % In this example we estimate a model without the seasonal component % 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960 y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan 118 126 150 180 196 188 233 277 301 318 342 391 % Feb 132 141 178 193 236 235 267 317 356 362 406 419 % Mar 129 135 163 181 235 227 269 313 348 348 396 461 % Apr 121 125 172 183 229 234 270 318 355 363 420 472 % May 135 149 178 218 243 264 315 374 422 435 472 535 % Jun 148 170 199 230 264 302 364 413 465 491 548 622 % Jul 148 170 199 242 272 293 347 405 467 505 559 606 % Aug 136 158 184 209 237 259 312 355 404 404 463 508 % Sep 119 133 162 191 211 229 274 306 347 359 407 461 % Oct 104 114 146 172 180 203 237 271 305 310 362 390 % Nov 118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec y=y(:); % Contaminate the first 20 observations y(1:20)=y(1:20)+200; % Model with linear trend and no seasonal component. Search for a level shift model=struct; model.trend=1; % linear trend model.s=12; % monthly time series model.seasonal=0; % no seasonal component model.lshift=10:(length(y)-10); % search for level shift out=LTSts(y,'model',model,'plots',1,'dispresults',true,'msg',0); % 3 years forecasts nfore=36; StartDate=[1949 1]; conflev=0.999; % Wide confidence level for the forecast outFORE=forecastTS(out,'model',model,'nfore',nfore,'StartDate',StartDate,'conflev',conflev);

Coeff SE t pval

_______ ________ _______ __________

b_trend1 307.43 7.2337 42.5 2.8696e-82

b_trend2 2.3919 0.087445 27.354 3.0083e-58

b_lshift -214.71 9.7761 -21.963 2.3563e-47

Level shift position t=21

Forecast with autoregressive components and expl var.

Forecast with autoregressive components and expl var.Simulated data with linear trend, varying seasonal and AR(2)

rng(1000) model=struct; model.trend=1; model.trendb=[5,1000]; model.seasonal=102; model.seasonalb=100*[2 4 0.1 8 0.001]; model.signal2noiseratio=10; model.ARp=[1 2]; model.ARb=[0.2 0.7]; model.ARIMAX=true; T=100; out=simulateTS(T,'model',model,'plots',1); % Fit a model imposing linear trend, seasonal component and AR(2) y=out.y; nfore=20; Xall=1e+2*randn(T+nfore,1); X=Xall(1:T,:); model=struct; model.trend=1; model.seasonal=102; % No level shift model.lshift=0; % Add a non important expl. variable model.X=X; model.ARp=[1 2]; out=LTSts(y,'model',model,'plots',1,'dispresults',true); % Note that in this case all the 120 values of Xall are supplied and % the number of forecasts is 20 model.X=Xall; forecastTS(out,'model',model,'nfore',20)

Iterative search of sigmaeps depending on the desired signal2noise ratio.

After 1000 iterations, the value of signal2noise ratio closest to the desired one is 10.0005,

obtained with sigmaeps = 107955.6243

Coeff SE t pval

_________ _________ ________ __________

b_trend1 -16801 33939 -0.49503 0.62178

b_trend2 2117.5 953.27 2.2214 0.028835

b_cos1 -32427 21648 -1.4979 0.13766

b_sin1 51362 27551 1.8642 0.065548

b_cos2 6181.2 16773 0.36852 0.71335

b_sin2 -39328 22569 -1.7426 0.084824

b_auto 1 0.16847 0.064852 2.5978 0.01096

b_auto 2 0.64325 0.065699 9.7907 7.7762e-16

b_explX1 360.92 157.24 2.2954 0.024035

b_varaml 0.0016604 0.0088853 0.18687 0.85218

ans =

struct with fields:

signal: [120×1 double]

trend: [120×1 double]

seasonal: [120×1 double]

X: [100×10 double]

lshift: 0

XAR: 0

Xexpl: [120×1 double]

confband: [120×2 double]

datesnumeric: [120×1 double]

Input Arguments

Output Arguments

References

Rousseeuw, P.J., Perrotta D., Riani M. and Hubert, M. (2018), Robust Monitoring of Many Time Series with Application to Fraud Detection, "Econometrics and Statistics". [RPRH]

See Also

LTSts

|

wedgeplot

|

simulateTS

|

LTStsVarSel