FM_spot_vol

FM_spot_vol computes the spot volatility of a diffusion process via the Fourier-Malliavin estimator

Syntax

Description

Examples

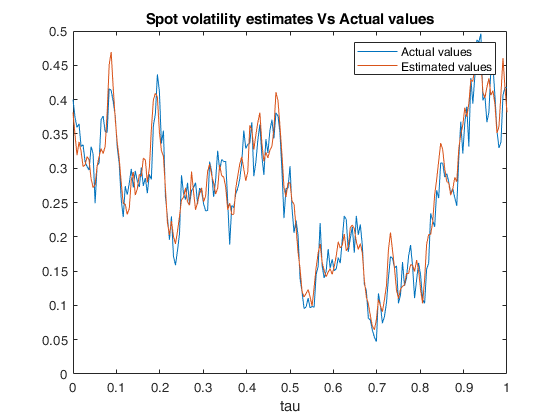

Example of call of FM_spot_vol with default values of M,N and tau.

Example of call of FM_spot_vol with default values of M,N and tau.

Example of call of FM_spot_vol with default values of M,N and tau.The following example estimates the path of the spot volatility of a Heston model from a discrete sample. The Heston model assumes that the spot variance follows a Cox-Ingersoll-Ross model.

% Heston model simulation

T=1;

n=23400;

parameters=[0,0.4,2,1];

Rho=-0.5;

x0=log(100);

V0=0.4;

[x,V,t]=Heston1D(T,n,parameters,Rho,x0,V0);

% Spot volatility estimation

[V_spot, tau_out]=FM_spot_vol(x,t,T);

M=(length(V_spot)-1)/2;

figure

plot(tau_out,V(1:round(n/(2*M)):end));

hold on

plot(tau_out,V_spot);

xlabel('tau');

title('Spot volatility estimates Vs Actual values')

legend('Actual values','Estimated values')

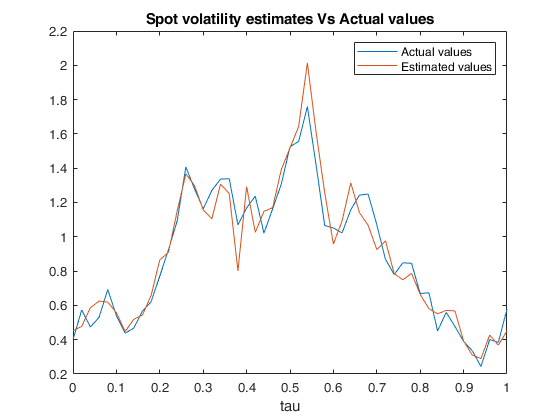

Example of call of FM_spot_vol with custom choices of M,N and tau.

Example of call of FM_spot_vol with custom choices of M,N and tau.The following example estimates the path of the spot volatility of a Heston model from a discrete sample. The Heston model assumes that the spot variance follows a Cox-Ingersoll-Ross model.

% Heston model simulation

T=1;

n=23400;

parameters=[0,0.4,2,1];

Rho=-0.5;

x0=log(100);

V0=0.4;

[x,V,t]=Heston1D(T,n,parameters,Rho,x0,V0);

% Spot volatility estimation

tau=0:T/50:T;

[V_spot, tau_out]= FM_spot_vol(x,t,T,'N',5000,'M',100,'tau',tau);

figure

plot(tau_out,V(1:round(n/50):end));

hold on

plot(tau_out,V_spot);

xlabel('tau');

title('Spot volatility estimates Vs Actual values')

legend('Actual values','Estimated values')

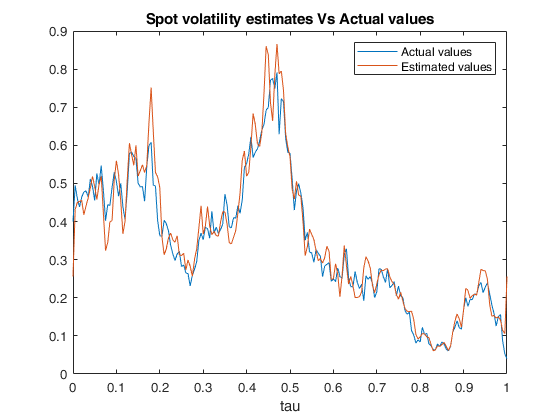

Example of call of FM_spot_vol when tau has length larger than 2M + 1.

Example of call of FM_spot_vol when tau has length larger than 2M + 1.The following example estimates the path of the spot volatility of a Heston model from a discrete sample. The Heston model assumes that the spot variance follows a Cox-Ingersoll-Ross model.

% Heston model simulation

T=1;

n=23400;

parameters=[0,0.4,2,1];

Rho=-0.5;

x0=log(100);

V0=0.4;

[x,V,t]=Heston1D(T,n,parameters,Rho,x0,V0);

% Spot volatility estimation

tau=0:T/1000:T;

[V_spot, tau_out]= FM_spot_vol(x,t,T,'N',5000,'M',100,'tau',tau);

figure

M=100;

plot(tau_out,V(1:round(n/(2*M)):end));

hold on

plot(tau_out,V_spot);

xlabel('tau');

title('Spot volatility estimates Vs Actual values')

legend('Actual values','Estimated values')WARNING: estimation will be performed on the equally-spaced grid with mesh size equal to T/(2*M), provided as an output variable.

Input Arguments

Output Arguments

More About

References

Mancino, M.E., Recchioni, M.C., Sanfelici, S. (2017), Fourier-Malliavin Volatility Estimation. Theory and Practice, "Springer Briefs in Quantitative Finance", Springer.

Sanfelici, S., Toscano, G. (2024), The Fourier-Malliavin Volatility (FMVol) MATLAB toolbox, available on ArXiv.

See Also

FE_spot_vol

|

FE_spot_vol_FFT

|

FM_spot_quart

|

FM_spot_volvol

|

FM_spot_lev

|

Heston1D