|

regressHhar |

removeExtraSpacesLF |

|

regressts

regressts computes estimates of regression parameters for a time series models

Description

Examples

regressTS with all the default options.

regressTS with all the default options.

regressTS with all the default options.Load airline data.

% 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960

y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan

118 126 150 180 196 188 233 277 301 318 342 391 % Feb

132 141 178 193 236 235 267 317 356 362 406 419 % Mar

129 135 163 181 235 227 269 313 348 348 396 461 % Apr

121 125 172 183 229 234 270 318 355 363 420 472 % May

135 149 178 218 243 264 315 374 422 435 472 535 % Jun

148 170 199 230 264 302 364 413 465 491 548 622 % Jul

148 170 199 242 272 293 347 405 467 505 559 606 % Aug

136 158 184 209 237 259 312 355 404 404 463 508 % Sep

119 133 162 191 211 229 274 306 347 359 407 461 % Oct

104 114 146 172 180 203 237 271 305 310 362 390 % Nov

118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec

y=(y(:));

% linear trend + just one harmonic for seasonal

out=regressts(y);

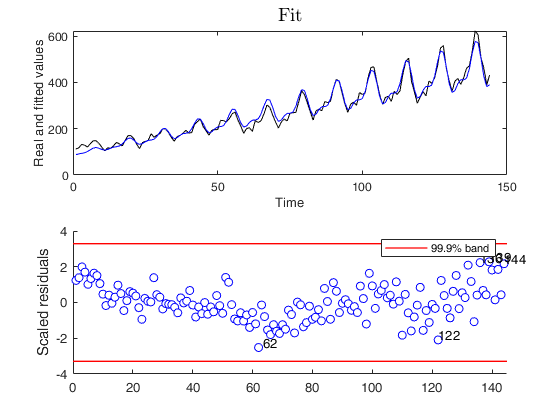

Example of the use of input option model and plots.

Example of the use of input option model and plots.Model with linear trend, two harmonics for seasonal component and varying amplitude using a linear trend.

% Load airline data.

% 1949 1950 1951 1952 1953 1954 1955 1956 1957 1958 1959 1960

y = [112 115 145 171 196 204 242 284 315 340 360 417 % Jan

118 126 150 180 196 188 233 277 301 318 342 391 % Feb

132 141 178 193 236 235 267 317 356 362 406 419 % Mar

129 135 163 181 235 227 269 313 348 348 396 461 % Apr

121 125 172 183 229 234 270 318 355 363 420 472 % May

135 149 178 218 243 264 315 374 422 435 472 535 % Jun

148 170 199 230 264 302 364 413 465 491 548 622 % Jul

148 170 199 242 272 293 347 405 467 505 559 606 % Aug

136 158 184 209 237 259 312 355 404 404 463 508 % Sep

119 133 162 191 211 229 274 306 347 359 407 461 % Oct

104 114 146 172 180 203 237 271 305 310 362 390 % Nov

118 140 166 194 201 229 278 306 336 337 405 432 ]; % Dec

y=(y(:));

model=struct;

model.trend=1; % linear trend

model.s=12; % monthly time series

model.seasonal=102; % two harmonics with time varying seasonality

out=regressts(y,'model',model,'plots',1);

Related Examples

Input Arguments

Output Arguments

References

Rousseeuw, P.J., Perrotta D., Riani M. and Hubert, M. (2018), Robust Monitoring of Many Time Series with Application to Fraud Detection, "Econometrics and Statistics". [RPRH]

|

|

regressHhar |

removeExtraSpacesLF |

|

|

|

Functions |

|

• The developers of the toolbox • The forward search group • Terms of Use • Acknowledgments